Rami Hajjar considers currency dynamics in emerging and frontier markets, focusing on how currency impacts returns, and how we think about this factor when investing in those markets. He also looks at South Africa in the context of the analysis and discusses whether the rand faces similar risks.

Given that emerging and frontier market currencies have weakened considerably over the recent past, this seems to be an opportune time to discuss some concerns investors have about investing in these markets.

Emerging and frontier markets are developing countries typically characterised by less mature capital markets, infrastructure and governance. This means that they tend to have less stable macroeconomic pillars in place: In most cases the tax take is low, governments spend beyond their means and, more importantly, there is a lack of institutional independence. Monetary policy is often at the service of the government, and fiscal and monetary profligacy tends to be correlated. These factors drive high currency volatility.

Recurrent macroeconomic and currency shocks do pose a problem in that they often cause short-term value loss … but these generally correct over time …

Focusing on currency performance

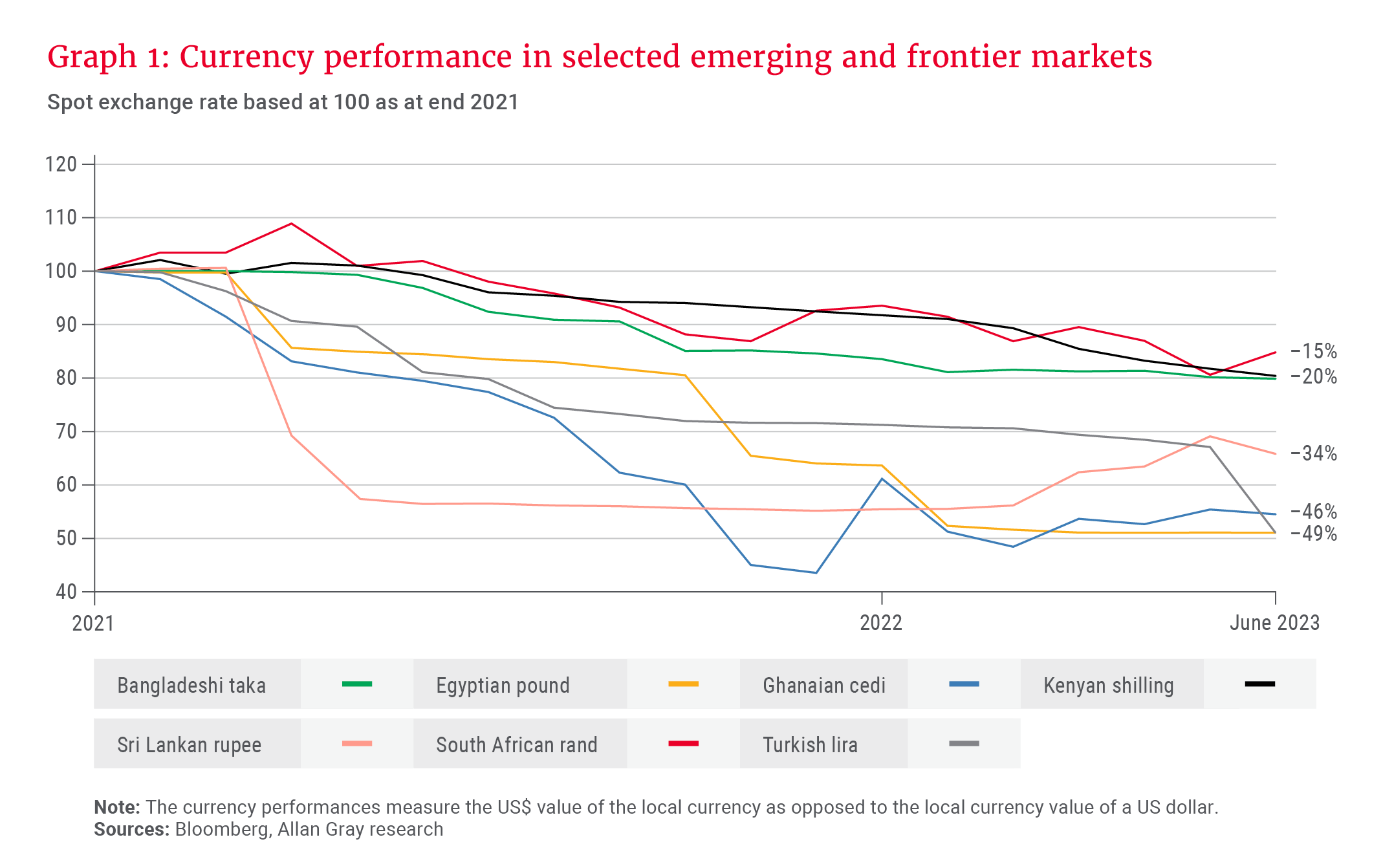

Since the end of 2021, several countries in emerging and frontier markets have experienced sizeable devaluations of their currencies, as shown in Graph 1. Large capital movements into and out of these markets are recurrent and generally track the developed markets’ economic cycle. High inflation has pushed developed markets’ central banks to increase interest rates, which, in turn, has reduced the relative attractiveness of returns in emerging and frontier markets. Some countries – many in the emerging and frontier universe – are more vulnerable, such as those with higher foreign currency debt levels and/or import needs, which exacerbate foreign exchange shortages and currency devaluation.

It is not an easy task to predict the timing or the magnitude of these moves. But once they occur, investors become increasingly concerned and question the case for investing in emerging and frontier markets.

Why do emerging and frontier markets have volatile exchange rates?

Let’s start by considering some basic concepts that will inform the ensuing analysis:

Fundamentally, two factors drive monetary stability: In a closed economy, the money supply is a main determinant of monetary stability. The monetarist view holds that an increase in the money supply by more than real gross domestic product (GDP) is inflationary.

In an open economy, money supply also drives monetary stability, but the exchange rate is an additional factor. The quantity of foreign exchange that a country has to meet its foreign exchange needs is a main driver of the exchange rate, as is the quantity of foreign exchange held relative to the local money supply. All else being equal, both a shortage of foreign exchange in the country and an increase in money supply, can lead to a large currency devaluation.

One important economic theory postulates that the relative prices of goods and services between two countries should not vary over time. High inflation in a given country necessitates an equivalent currency devaluation to keep relative prices broadly intact. This appears to hold over long periods of time: Inflation and the exchange rate are very highly correlated. In economic jargon, this is referred to as the relative Purchasing Power Parity (PPP) model.

Money supply impacts inflation

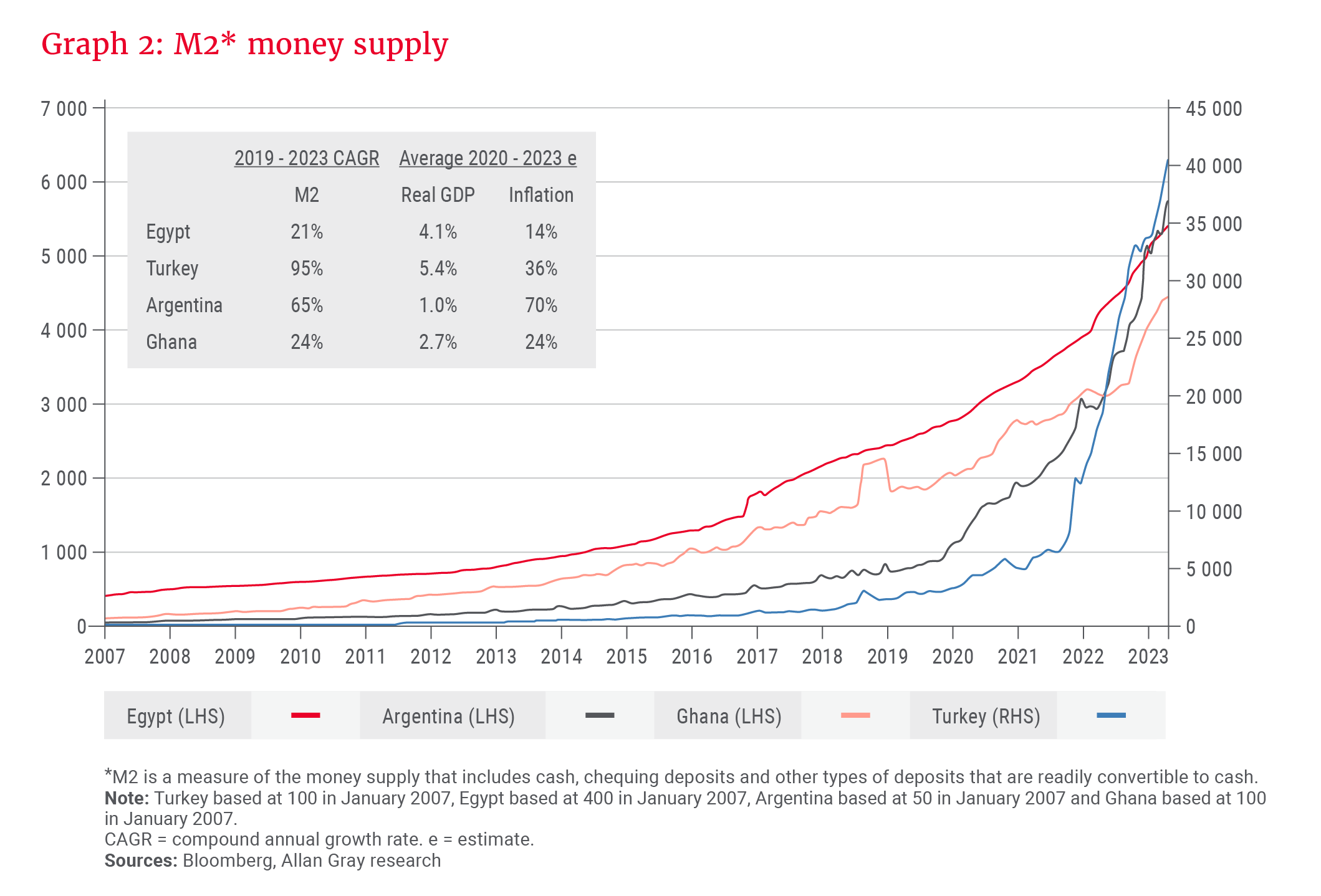

A common driver of large currency devaluations in emerging and frontier markets is very high inflation levels that are caused by large increases in the money supply. Let’s look at the example of four currencies that have experienced very large devaluations since the end of 2019: The Turkish lira is down 70%, the Egyptian pound 52%, the Argentinian peso 75% and the Ghanaian cedi 52%.

An increase in money supply through reckless monetary policy – which in most cases is tied to reckless fiscal policy – has led to very high inflation levels, as shown in Graph 2. This, in turn, has been a major factor behind the large currency devaluations.

Increase in money supply → Inflation → Currency devaluation

Importantly, those inflation levels and the concomitant currency trajectories are the result of arbitrary changes in monetary policy and not something that could have been assessed beforehand. If one can no longer reliably forecast inflation in a country, it becomes futile to determine the fair value of that country’s currency; or to be more specific, to anchor the US dollar value of a local currency today with the aim of establishing a trajectory that could be reliably forecast.

Foreign exchange reserves matter

Monetary policy is a large driver of the currency but is not the only factor at play. Irrespective of monetary policy, countries that lack a diversified export base (to earn foreign currency) or that have a strong reliance on the imports of goods (and have to pay foreign currency) are highly exposed to exogenous shocks. An unfavourable change in the terms of trade can lead to large shortages in foreign currency at times. For countries that haven’t built the appropriate foreign currency reserves (or are not fortunate enough to receive a large external bailout), the change in the exchange rate could become permanent: The inability to supply the necessary amount of foreign currency to meet local demand for foreign goods and services until circumstances normalise can lead to a currency devaluation/inflation spiral.

Currency devaluation → Inflation → Further devaluation

From a return perspective, do currency moves matter over long periods of time?

Currency moves in emerging and frontier markets impact returns for foreign investors. Stocks and interest-bearing securities have local currency income streams, and the US dollar prices of those securities move in tandem with the US dollar value of those streams.

Interest-bearing securities

Interest-bearing securities include T-bills, bonds and any form of local currency debt. From a foreign investor’s standpoint:

Returns = nominal yield + currency change over the investment period

Given the fixed nature of the income stream, large currency devaluations have a significant impact on returns.

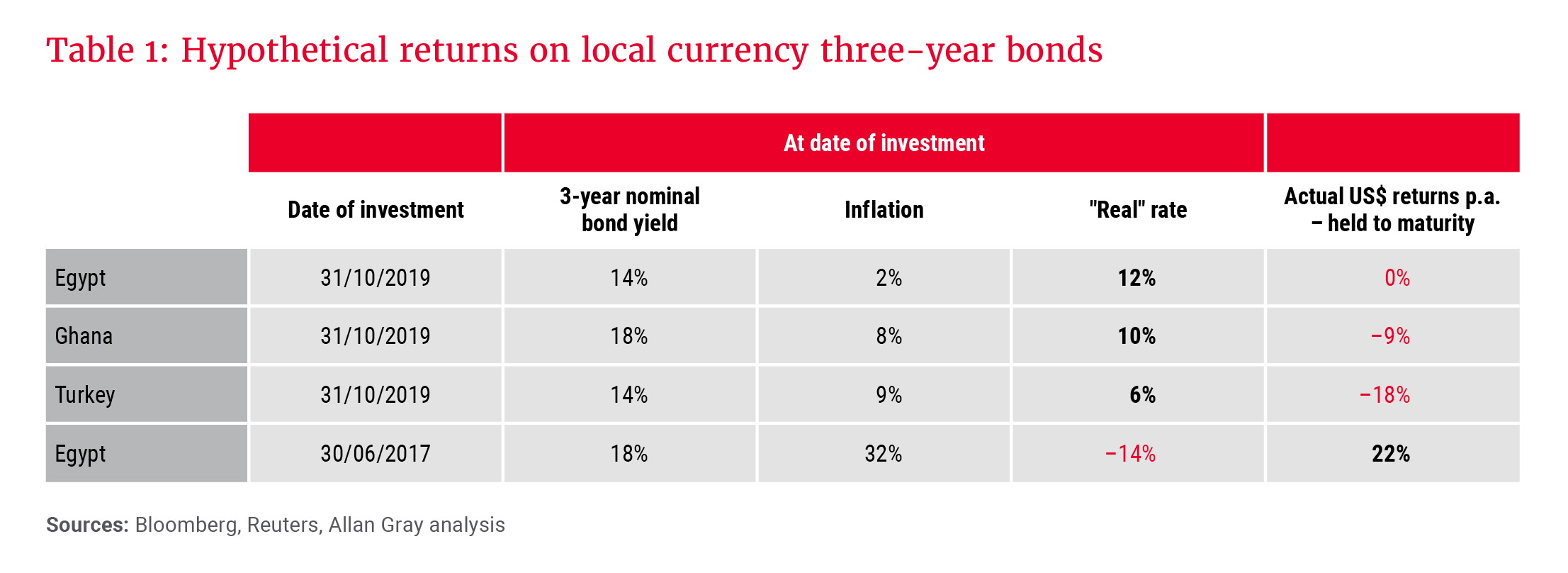

A metric often used to gauge the attractiveness of a local currency interest-bearing security is the real (after local inflation) yield. The problem with this metric is that it uses current local inflation as a deflator to determine the approximate real return. In countries with stable macroeconomics, inflation expectations are more predictable, and this metric can be relied on to some extent (the real rate should approximate the US dollar return). But this is not the case in countries with mismanaged macroeconomic policy or countries at high risk of exogenous shocks. Table 1 provides good examples.

The disconnect between inflation at the date of investment and actual currency devaluation over three years meant that while real rates screened attractive towards the end of 2019, the actual returns were very poor. In contrast, in June 2017, while real rates on Egyptian bonds were deep in the negative, an investor in those bonds would have generated 22% p.a. in US dollars over the next three years.

As bond investors in these markets, we proactively gauge the likelihood of upcoming shocks and position our portfolios accordingly. For instance, since the double whammy of COVID-19 and the Russia-Ukraine war, we have tilted the Allan Gray Africa Bond Fund substantially into Eurobonds and kept a small exposure to locally denominated instruments in countries with much lower risk of currency shocks, such as Uganda.

Stocks

Over long periods of time, the value of a stock is driven by the earnings that the company generates – and earnings are a function of the prices a company can charge for its goods and services.

On aggregate, corporates price with inflation – which is nothing but the change in the aggregate price level of goods and services that corporates sell. Based on the relative PPP model and what history suggests, currency devaluation and inflation tend to move in tandem, which means that the real value of a corporate’s revenue stream or profits should be protected over time.

However, reality over the short term is not as smooth as long-term trends. Firstly, currency devaluation has a direct translation impact on today’s earnings. Given that the market is short-term-driven, this impacts short-term price performance. Secondly, adjustments take time, and short-term problems arise that can lead to longer-term ones. Some of the more common issues include a large deterioration in the purchasing power of consumers, which does not recover quickly, an inability to pass cost increases on to consumers for some time, currency mismatches on the balance sheet, and the inability to source foreign exchange.

… [quality] corporates tend to restore their earning power quickly, thereby providing a natural hedge to currency devaluation.

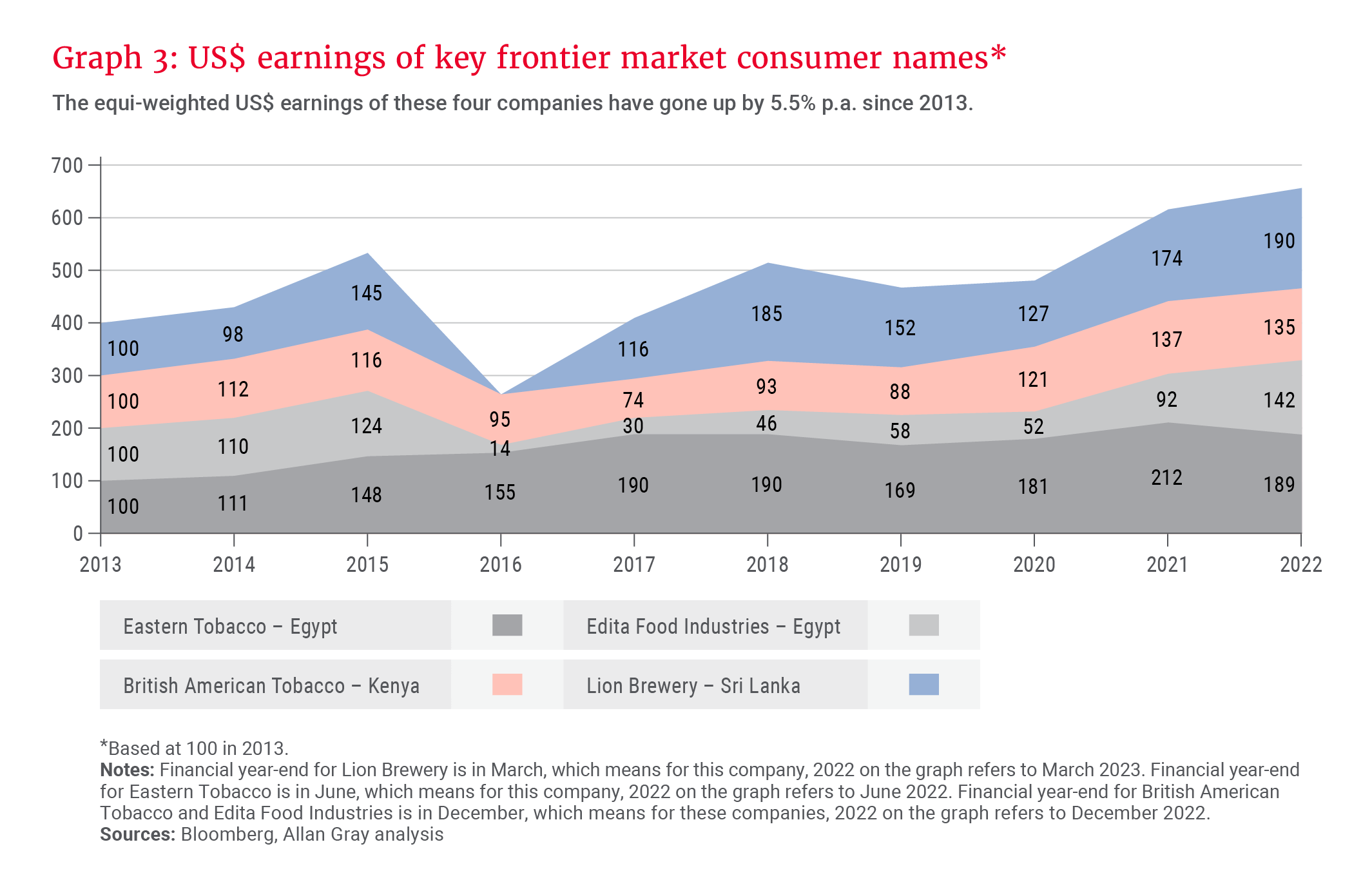

Given the recurring nature of macroeconomic shocks, many of the quality corporates in those countries have developed resilient business models and are accustomed to those risks. These corporates tend to restore their earning power quickly, thereby providing a natural hedge to currency devaluation. As investment managers, we strive to pick those quality stocks. Graph 3 depicts the earnings of four names we hold on behalf of our clients.

Despite large currency devaluation in their respective countries, these consumer names – whose earnings are predominantly in local currency – have seen decent US dollar profit growth since 2013. And it is US dollar earnings growth that drives share price performance over time.

How to think of value amid high currency volatility: The case of Zimbabwe

Zimbabwe provides an extreme example to explain how we think of value in markets with high currency volatility. I will not expand on Zimbabwe’s economic case in this piece. Suffice to say that highly reckless fiscal and monetary policies have led to repeated episodes of monetary debasement since 2000 – reflected in multiple periods of hyperinflation and currency collapses.

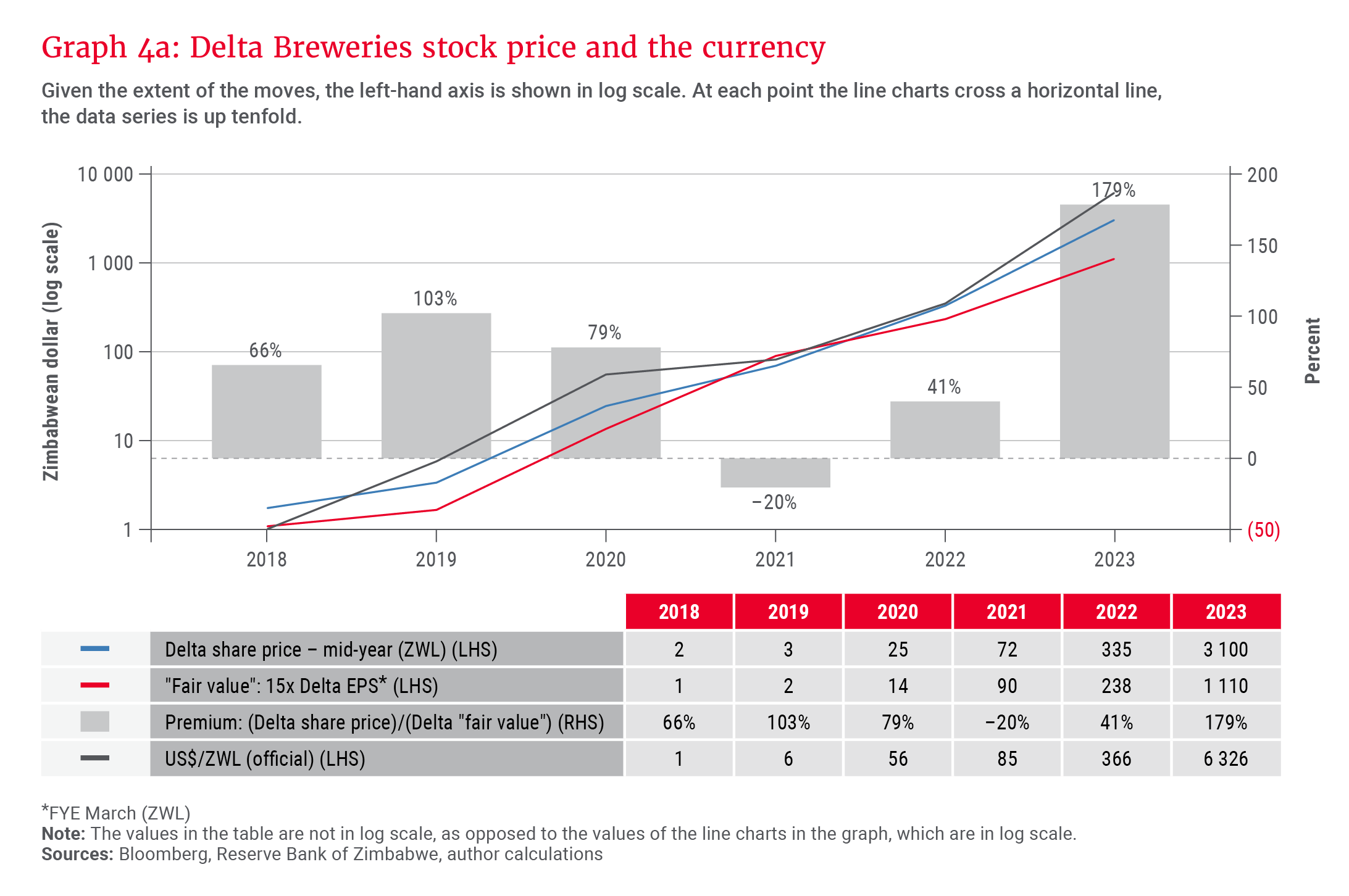

Let’s take the example of the dominant brewer in Zimbabwe, Delta Breweries. As Graph 4a shows, there is a clear positive correlation between Delta’s earnings in Zimbabwean dollar (ZWL), the stock price and the foreign exchange rate.

Local currency earnings at a given point in time do not tell us much and looking at local currency valuations is not appropriate in such circumstances. For instance, valuing Delta using 15 times end of March 2023 earnings per share would yield a fair price of ZWL1 110. Spot price on 30 June 2023 was ZWL3 147 (Graph 4a, bar chart, right-hand-side axis, depicts the large premium of the spot rate relative to a conventional approach to calculate fair value).

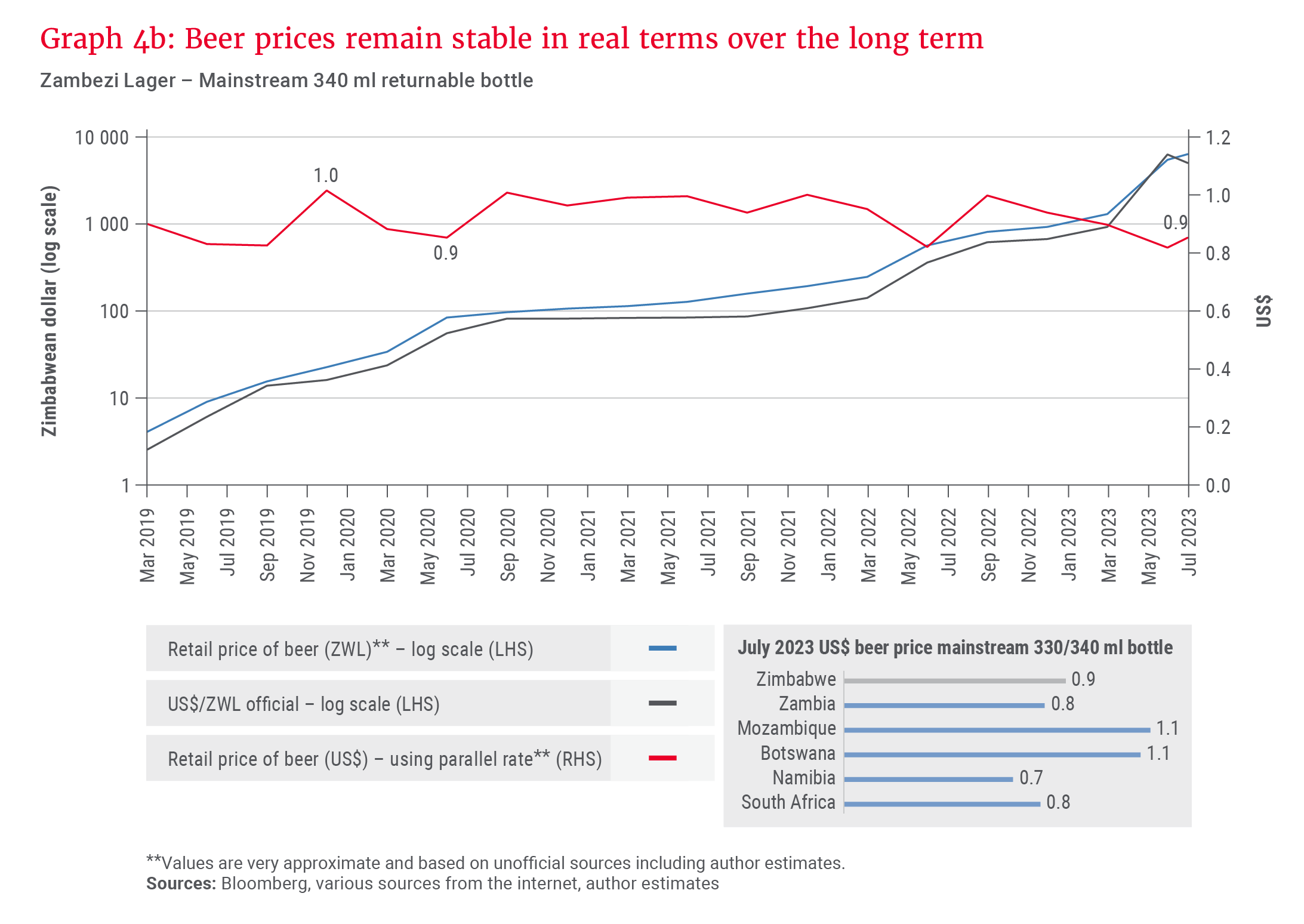

The aim is to anchor the net worth of a business to a stable value. Delta is a dominant brewer that owns state-of-the-art equipment (real assets), sells products that are in strong demand throughout the cycle, and proactively prices its products with inflation. As Graph 4b shows, the US dollar price of a beer in Zimbabwe at any given point in time does not differ much relative to history and remains in a range that is comparable to prices in the region. One can therefore make assumptions about the US dollar earning power of the business – irrespective of whether the company is generating US dollar or Zimbabwean dollar revenues.

Once conservative assumptions are made, one can estimate the net worth of the business by applying the right valuation multiple. In situations where value is not realisable, such as is the case with Zimbabwe today, we apply a further discount to the valuation multiple. In fact, our positions in Zimbabwe are valued at the lower of the market price, using the official exchange rate, or our conservative estimate of each stock’s fair value.

Patient investors can earn real returns

We generally avoid making firm currency forecasts. On the one hand, this is not our speciality, and the track record of those who do it is mixed. On the other, we try to think of valuations irrespective of currency moves.

This doesn’t mean that we do not consider the country’s track record in macroeconomic governance and its history of monetary management. Recurrent macroeconomic and currency shocks do pose a problem in that they often cause short-term value loss (lower US dollar earnings and dividends), but these generally correct over time, and patient investors are able to generate decent real returns.

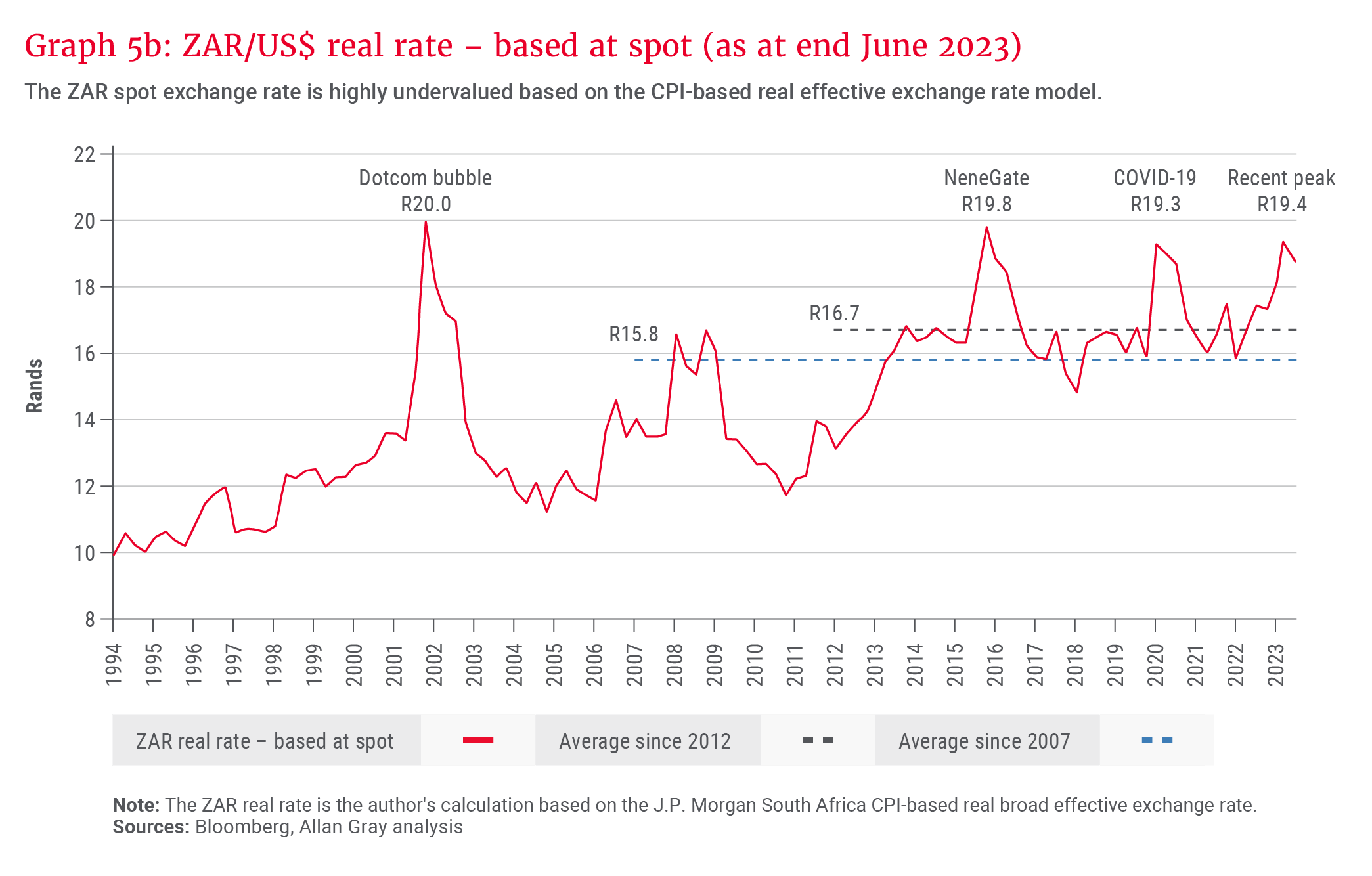

Is South Africa at risk of currency debasement?

One important takeaway from the countries we considered is that reckless fiscal and monetary policies have led to very high inflation levels, and these have been the main drivers of the currency collapses.

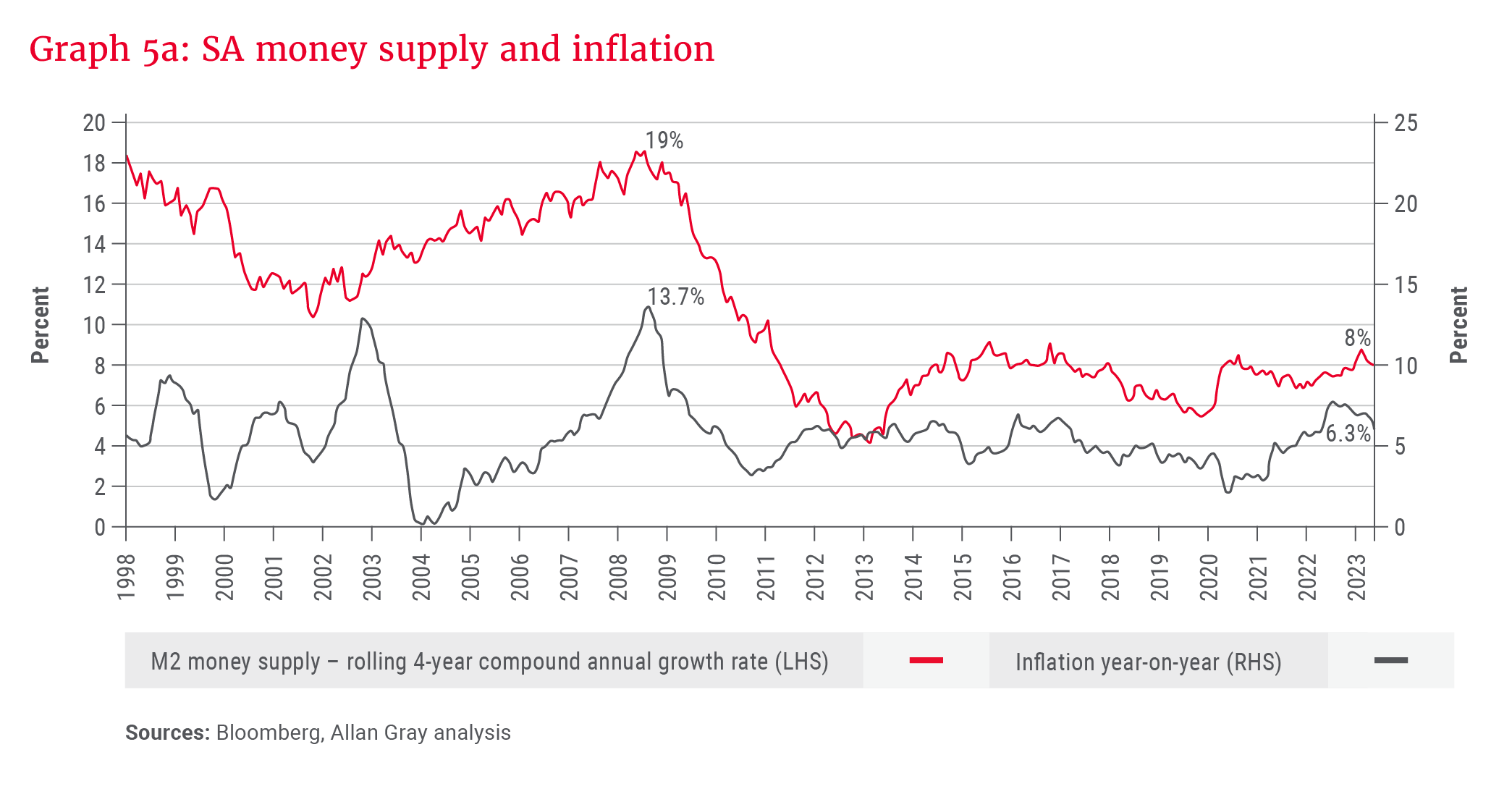

Graph 5a shows that South Africa has a good track record of monetary discipline. This is one benefit of having an independent central bank that respects a mandate to control inflation. Continued monetary discipline and anchored inflation expectations will be important drivers of currency stability going forward – while recognising that monetary policy can lose its effectiveness with fiscal imprudence.

The other fundamental factor in currency stability is foreign exchange supply and demand. South Africa has a structural current account deficit, which means that normal economic activity results in more foreign exchange going out of the country than coming in, in any given year. But the deficit is not large, and the country fares well relative to other markets we consider, as it has an export base that is sensitive to rand weakness, and some import substitution can take place when the currency weakens a lot – a natural adjustment mechanism. The latter factor means that the pass-through effect from the weakened currency to inflation is not very large, compared to that in a country like Egypt, for instance, where the local manufacturing base is very weak.

There is an important third factor to consider: confidence. No matter how solid the fundamentals of a country are, investors losing confidence in a market can drive a run on the currency. In such a scenario, a dangerous feedback loop can kick in where negative sentiment drives currency drops, and large currency drops start to de-anchor inflation expectations, which causes further currency drops.

The probability of this happening in South Africa is low, and we are hopeful that the action plan currently in place to solve the crucial infrastructure issues, together with successful efforts to contain the fiscus, will prompt a re-evaluation of South Africa’s investment case.