The end of the tax year in February presents an opportunity to evaluate the tax efficiency of your financial plan. With many competing financial priorities in the current economic climate, as well as the pending changes to the retirement fund system, you may be wondering whether maximising the annual tax incentives still makes sense. Carla Rossouw unpacks the benefits of retirement annuities and tax-free investments, looks at how much to contribute, and discusses the trade-offs to consider when choosing a product.

Incorporating retirement funds (pension funds, provident funds and retirement annuities (RAs)) and tax-free investments (TFIs) into your long-term investment strategy can improve your chances of retiring comfortably and increases the amount of financial flexibility you have before and at the point of retirement.

For the purposes of this discussion, we look at RAs and TFIs. While there are tax benefits associated with both, the benefits are structured differently, and the product rules and restrictions are quite distinct. Depending on your goals and objectives, there may be a place for both products in your investment portfolio. A good, independent financial adviser can help you understand the benefits and trade-offs and decide which products are best for your circumstances.

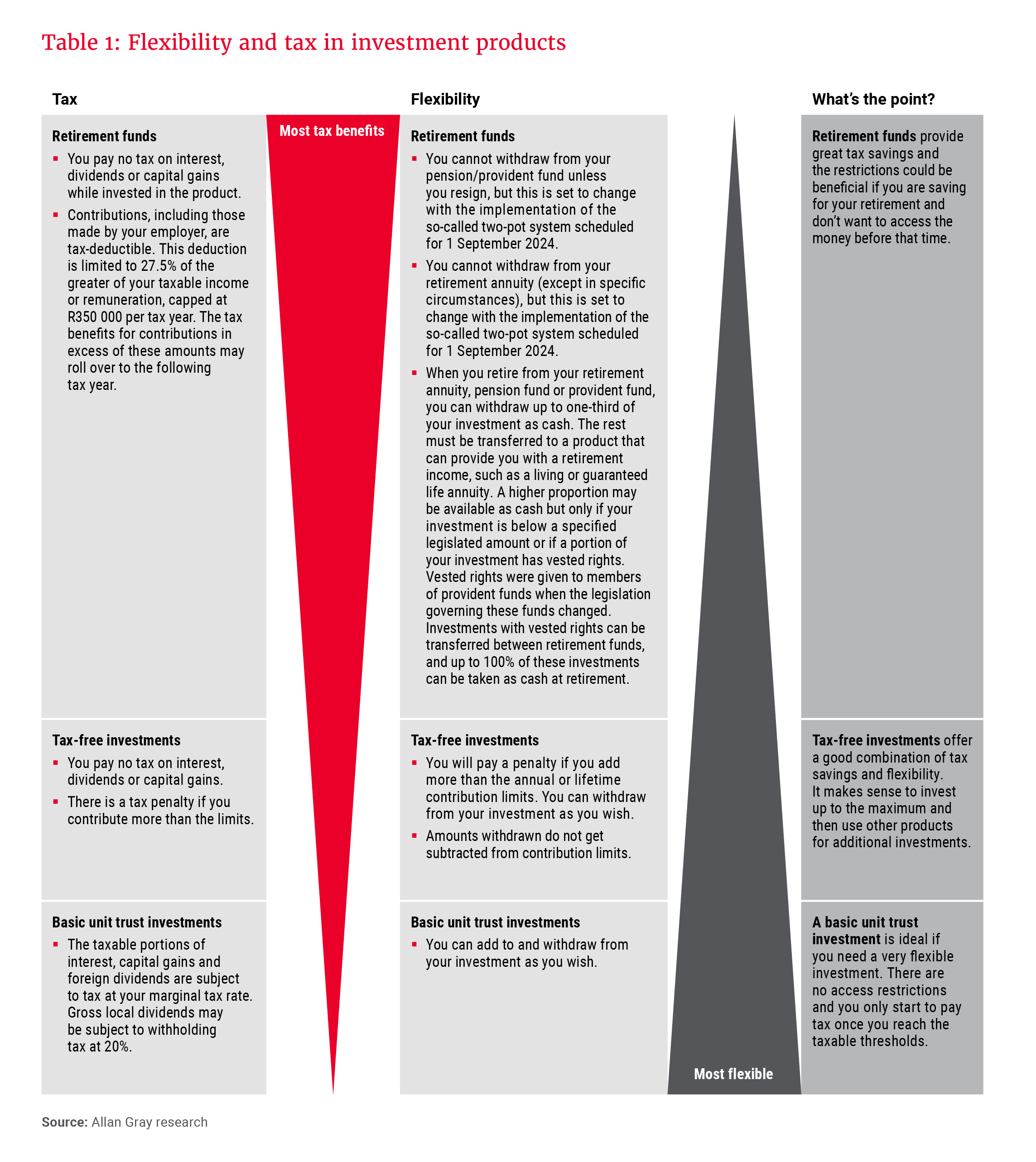

Different products have different advantages and disadvantages … and tax efficiency cannot be looked at in isolation – you also need to consider each product’s suitability and flexibility.

Focusing on retirement annuities

While pension and provident funds are made available through an employer, either in the form of their own fund or an umbrella fund, an RA is a retirement savings product that investors can hold in their personal capacity. RAs are not linked to employment, and are a good mechanism for saving for retirement for those who are self-employed or those looking to supplement their employer’s arrangement.

Tax benefits

RAs offer tax savings now, i.e. you pay less tax now because you make contributions with earnings on which you have not paid tax. However, you will pay tax when you retire and draw an income (although this will likely be at a lower rate than your current tax rate). Your tax saving now directly correlates with your marginal tax rate, therefore the higher your marginal tax rate, the greater the tax saving on your RA contributions before retirement.

You can claim a tax deduction for contributions to all retirement funds, subject to a legislated maximum of the greater of 27.5% of taxable income or remuneration, capped at R350 000 per tax year (although there are benefits, rather than penalties, if you exceed this maximum, as discussed in the “Excess contributions are beneficial” section). While you naturally come out with less take-home pay per month if you increase your RA contributions to enjoy the maximum tax benefit, a smaller portion of your salary goes to the tax man.

Graph 1 illustrates this principle through an example of an individual earning R480 000 per year making contributions to an RA at different levels. The graph shows that the amount of tax you pay decreases as your contribution increases: If the individual in the example contributes nothing to an RA, they pay 23% of their gross monthly salary in tax, which goes down to 19% when they make a 15% contribution, and to as low as 15% when they contribute 27.5% of their salary.

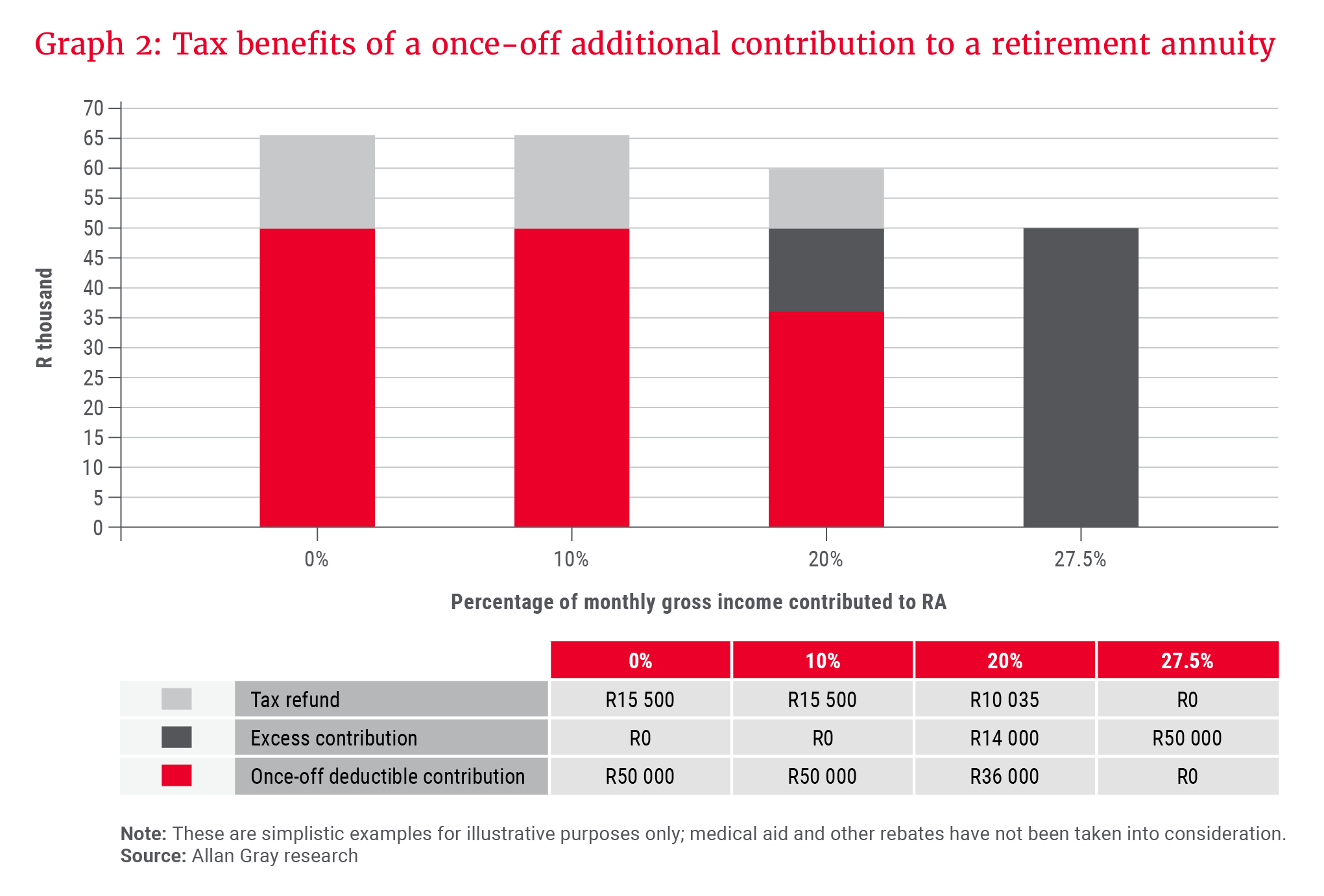

Taxpayers also have the option to make once-off additional contributions to an RA within a particular tax year. You can consider this approach if you prefer to maintain a certain level of disposable income throughout the year by keeping your monthly RA contributions at a minimum. An additional contribution can further decrease your taxable income and may result in a tax refund, as shown in Graph 2.

Remember, annual tax benefits are forfeited if you don’t make use of them before the deadline.

Using the same inputs as in Graph 1, Graph 2 illustrates the tax benefits of making an additional contribution of R50 000 at the end of the tax year. The graph shows that this will result in a tax refund, as the taxpayer has effectively overpaid pay-as-you-earn (PAYE) tax. It also shows that if no contribution was made during the year, and a R50 000 once-off contribution was made at tax year-end, the taxpayer would be due a R15 500 refund. The refund is lower for those who contribute from their salaries during the year, as they have already received the tax benefit (contributions are made before tax is calculated).

If a taxpayer is already contributing a significant portion of their monthly salary – 20% or higher – to an RA, the legislated limits are applied. At this point, any contribution in excess of 27.5% will be treated as an “excess contribution” and carried over to future tax periods (as discussed below).

Like many countries, South Africa has a progressive personal income tax regime, with our tax rates placing a heavier tax burden on the highest earners. If you earn above the highest tax bracket, you will save 45% in tax on every extra rand saved in an RA if it is under the annual rand cap on deductions. Not everyone can afford to save 27.5% of their income towards retirement, but the more you save, the better your position will be in retirement.

your extra … contributions … can benefit you throughout your lifetime.

In addition to the tax break on contributions, you pay no tax on the interest, capital gains or dividends you earn while invested. Meanwhile, the first R550 000 lump sum you take at retirement is currently tax-free (importantly, this amount includes all previous taxable lump sums received from any other retirement fund or an employer as a severance benefit).

An RA also provides estate duty advantages: When you die, an RA doesn’t form part of your estate, which means it will not attract estate duty. However, excess contributions that have been allowed as a deduction to determine the taxable portion of the cash lump sum benefit on death are included in the value of property of the deceased for the purposes of determining estate duty.

Excess contributions are beneficial

If you contribute more than the annual limit, your extra, after-tax (non-deductible) contributions (excess contributions) can benefit you throughout your lifetime: They can be carried over and deducted in the next year, and they continue to be carried over until they are fully utilised – so the benefit is never lost.

Excess contributions can be used to:

- Increase the value of any tax-free lump sum you take before or at retirement

- Reduce the taxable portion of your living annuity income in retirement

- Reduce the taxable portion of any lump sum your beneficiaries choose to take as cash on your death

Calculation 1 illustrates how the South African Revenue Service (SARS) calculates your tax liability on the cash lump sum at retirement, and how excess contributions can save you tax.

The calculation assumes that:

- You have not taken any previous taxable lump sums, therefore the R550 000 that is made available to you during your lifetime at 0% tax is still available

- You have R200 000 of excess contributions on record with SARS

- The market value of your RA is R2.4m and you choose to take one-third (R800 000) as cash

Calculation 1: How excess contributions can save you tax

Step one: Your cash amount to be taxed is first reduced by your excess contributions: R800 000 – R200 000 = R600 000

Step two: Apply the retirement tax table to the reduced cash amount: (R600 000 – R550 000) x 18% = R9 000

Result: Your final tax bill is R9 000.

Without your excess contributions, you would have paid significantly more as you would have paid tax on a larger amount:

Calculation 2: No excess contributions therefore no additional tax saving

Step one: No excess contributions, therefore no reduction.

Step two: Apply the retirement tax table to the lump sum of R800 000: (R800 000 – R770 000) x 27% + R39 600 = R47 700

Result: Your final tax bill is R47 700.

Restrictions to be aware of

As with most things in life, there are trade-offs. Some argue that the restrictions discussed below outweigh the various benefits of RAs:

Investment limits: Regulation 28 of the Pension Funds Act limits an investor’s exposure to certain asset classes. You can currently have a maximum of 75% exposure to equities and a 45% allocation offshore. These restrictions may not work for you. However, they are intended as a safeguard against asset allocation that may lead to volatile portfolio performance (which is often accompanied by poor investor behaviour).

Liquidity limits: To ensure that retirement fund investments are used for their intended purpose, there are rules that govern when and how you can access your nest egg. Except under certain circumstances, your RA cannot be withdrawn before retirement, and at retirement, your access to cash is limited.

Changes are imminent, with the implementation of the so-called two-pot system scheduled for 1 September 2024. From this date, all future contributions to pension funds, provident funds and RAs, including the Allan Gray Umbrella Retirement Fund and Allan Gray Retirement Annuity Fund, will be split into two components: One-third of the contributions will be credited to a savings component, and the remaining two-thirds will be credited to a retirement component.

At any point prior to retirement, members will be entitled to access a withdrawal of up to 100% of the amount that has been accumulated in the savings component, subject to a minimum withdrawal of R2 000. The retirement component will be inaccessible before you retire and, as per the current rules, must be used to purchase an income-bearing product in retirement, such as a living or guaranteed life annuity, which will provide you with an income after you retire.

It is also important to be aware that if you are ceasing tax residency in South Africa, you will only be able to access your RA or preservation fund benefits if you have not been a South African tax resident for an uninterrupted period of three years on or after 1 March 2021. Note that if you have not accessed your pre-retirement withdrawal benefit from your preservation fund, you will have immediate access to your benefit, as has always been the case.

Estate-planning limitations: RAs do not form part of your estate. Although you are encouraged to nominate beneficiaries to receive your benefit if you die while you are still invested in the product, the trustees of the fund are ultimately responsible for allocating your benefit.

Where do tax-free investments fit in?

A TFI is a great way to boost your savings and invest for the long term. Although you invest with after-tax money, you pay no tax on the interest, capital gains or dividends you earn, or on any withdrawals you make. The true benefit of a TFI is felt over the long term as tax-free returns compound.

There are, however, restrictions in terms of how much you can contribute, and the maximum amounts may not be enough for retirement. SARS allows taxpayers to save a maximum of R36 000 per tax year and R500 000 in your lifetime tax-free, and there are tax implications for overcontributing. Unlike the excess contribution treatment in RAs, you will incur a tax penalty of 40% on any amount over the contribution limits. This applies when you file your tax return, so you need to keep track of how much you’re contributing each year to your TFIs (across various service providers).

The true benefit of a TFI is felt over the long term as tax-free returns compound.

Many investors like TFIs because of their flexibility: Unlike in the case of RAs, there are no asset class restrictions, and you can access your investment at any point in time. However, any amount that you withdraw cannot be recontributed. While your TFI forms part of your estate, if it is structured as a life policy, as is the case with the Allan Gray Tax-Free Investment, the investment can be paid to your beneficiaries immediately, and there are no executor fees.

Product choices

Different products have different advantages and disadvantages, as we discussed in our Q2 2023 Allan Gray Quarterly Commentary, and tax efficiency cannot be looked at in isolation – you also need to consider each product’s suitability and flexibility. Table 1 summarises the role of RAs, TFIs and basic unit trust investments, along with their flexibility and tax rules.

It is not necessarily an either/or decision; combining an RA with a TFI might provide the best outcome from a liquidity and tax-saving perspective, since one may argue that it offers the best of both worlds. TFI accounts offer less tax savings and are capped at a lower amount, but are less restrictive.

From a retirement savings perspective considering the income provided in retirement, in most cases, RAs offer the best deal. However, you need to be able to live with the restrictions.

Maximise the benefits before the end of February

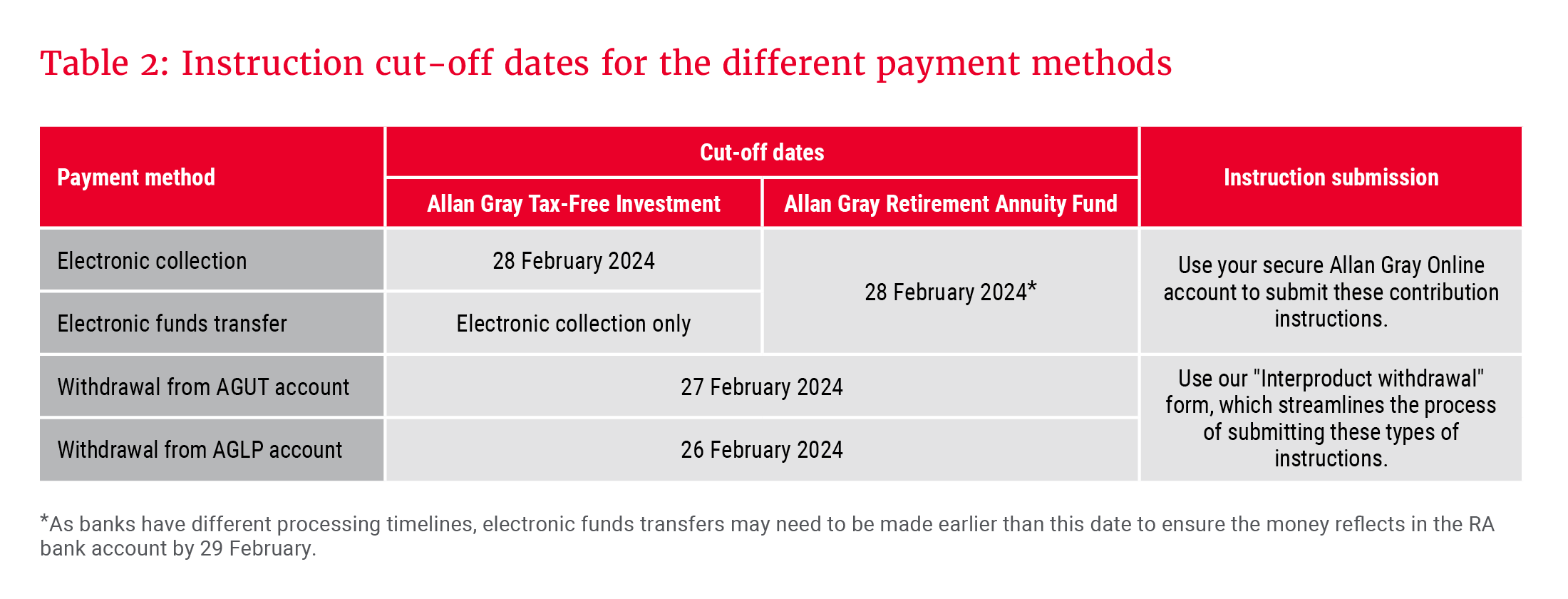

Remember, annual tax benefits are forfeited if you don’t make use of them before the deadline. The current tax year will come to an end on 29 February 2024.

If you are planning to make use of the tax concessions for the 2023/2024 tax year by starting a new RA or TFI, or by making an additional contribution to an existing account, please make sure we receive your instruction, supporting documents and payment well in advance of the deadlines shown in Table 2.