When it comes to managing your wealth, there’s a yawning gap between what personal finance pundits advocate and what economists believe. Who should you listen to? Earl Van Zyl, head of Retail Product Development, says both, without losing your common sense, of course.

Recent research by James Choi, finance professor at the Yale School of Management, says that there is a surprising disconnect between personal finance advice, which tends to take psychology into account, and economic theory, which operates in a purely rational world.

Choi researched the top 50 personal finance books on Goodreads, including classics such as Rich Dad, Poor Dad, and others by Suze Orman and Dave Ramsay, and observed how they compared with principles of economic theory.

Saving for your retirement

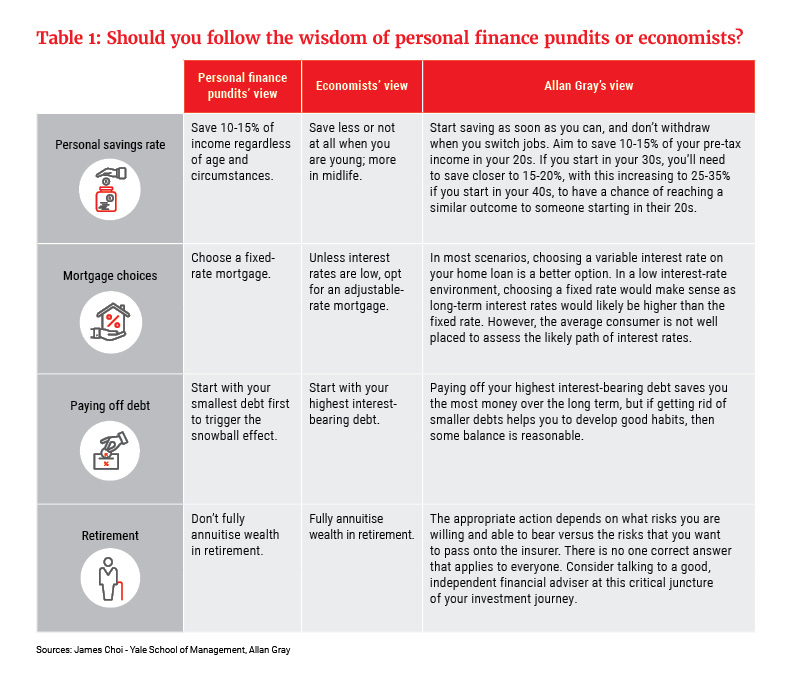

According to many personal finance experts, you should be saving 10-15% of your income for retirement to benefit from the magic of compound interest. That’s in stark contrast to economists, who say that you should invest in yourself when you’re young and start saving for your retirement later when you’re earning more.

I tend to agree with personal finance wisdom in this regard. Psychologists would point out that habits, whether good or bad, formed early in life tend to stick. While economic theory recommends saving more as you get older, the danger is that people not used to saving in their 20s and 30s will find it increasingly difficult to save a higher proportion of their income as they get older.

Should you fully annuitise wealth in retirement?

Another point of contention is whether to fully annuitise wealth in retirement or not. “Annuitising” refers to guaranteeing an income using some or all of your retirement savings pot. Retirees annuitise by using their accumulated retirement savings to purchase a guaranteed life annuity which, as the name suggests, will pay a guaranteed income or pension to the retiree for the rest of their life. These benefits come at the cost of little flexibility and low or no capital legacy on death. The other option is to purchase a living annuity. Here the retiree has more investment choice, control over their income and can leave any capital balance at their death to their beneficiaries – however, they have to be comfortable taking on investment and longevity risk – i.e., their investment could fall in value and they could outlive their income.

Personal finance pundits favour not fully annuitising, while economists opt for “all in” – there is seldom a “correct” answer in this debate. Here, the appropriate course of action very much depends on what risks the retiree would like to bear versus the risks that they want to pass onto the insurer.

Choosing not to annuitise any portion of your retirement savings by, for example, investing your retirement savings in a living annuity, may be appropriate if you can draw an income at a rate below the rate at which your living annuity capital will grow in real terms and if it is important to you to leave capital to your beneficiaries when you die.

If, on the other hand, you would prefer to pass on some of your future income risk to the insurer, you can guarantee or annuitise a portion of your retirement savings pot and supplement that guaranteed income with income from your remaining market-linked living annuity investment. In this scenario, you reduce your risk of running out of capital to sustain your basic income needs, but you leave some capital to pass onto your beneficiaries if you die with some portion of your investment remaining.

Table 1 reflects some of the differing views.

Who is “more” correct?

Why is there a wide gap between these two schools of thought? Because economists are not personal financial advisers. Their goal in developing simplified economic models of complex financial choices, and in making recommendations based on those models, is to recommend actions that will maximise economic wealth over the long term for individuals and households that behave entirely rationally. Similarly, personal finance “advice” delivered to broad groups also relies on rules of thumb and broad assumptions about how people behave.

As every individual has unique goals and appetite for risk, standard economic and personal finance insights must be adapted to account for personal circumstances. How well an investor will fare in the end is dependent on several factors, some of which – like behaviour – may be unpredictable.

What the research doesn’t cover: The behaviour penalty

Choi’s research, while fascinating, doesn’t cover a critical defining factor of investment success: investor behaviour. The so-called behaviour gap – the difference between the long-term return achieved by an investment fund and the return experienced by an individual investor – impacts most scenarios.

The behaviour gap is effectively a penalty that investors pay for making investment decisions based on emotional responses to changes in investment markets, such as switching between funds or withdrawing savings at inopportune times. We tend to disinvest when our investment is doing badly and invest after periods of high returns. Over time, this behaviour leads to investor returns being lower than what one would have achieved had you simply stuck to your original investment.

With so much conflicting information available, and the behaviour penalty to contend with, it is a good idea to consult a good, independent financial adviser. A seasoned financial adviser can help you devise a financial plan that takes your personal circumstances into account and makes you aware of the trade-offs that you are making when you deviate from standard economic models.