Investors who emigrate are often surprised by the complexity involved in accessing their existing retirement investments after they have ceased to be South African tax residents. Although double taxation agreements can provide much-needed relief from South African tax on retirement income, navigating these benefits often proves challenging. Meagan Fraser provides answers to some frequently asked questions.

Many South Africans who decide to emigrate permanently and formally cease their South African tax residency with the South African Revenue Service (SARS) find that they are unable to access their retirement investment immediately upon departure. There are various options available to you once you become a non-resident, and understanding the tax implications of accessing your retirement investment ensures informed decision-making.

How much of my retirement investments can I access when I leave the country before retirement age?

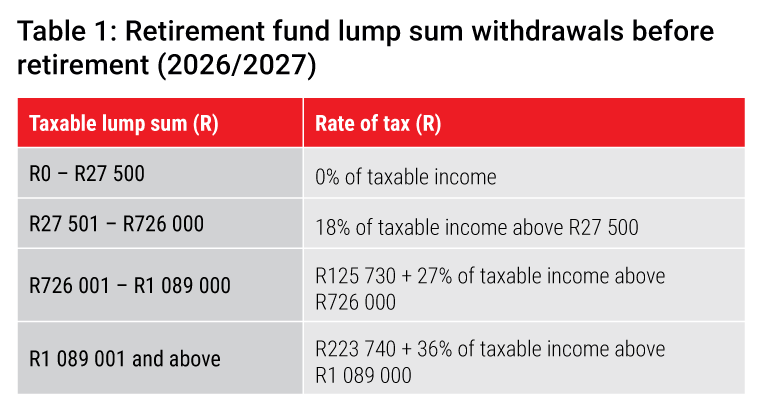

When emigrating, it is imperative that you inform SARS as soon as you cease to be a South African tax resident. As a non-resident, you will be able to withdraw from the savings component of your retirement investments at any point in time, and these withdrawals will be taxed at your South African marginal tax rate. You may also choose to transfer the value in your savings component to your retirement component, if you wish to access the amount in your retirement component through a cessation of residence withdrawal. If you have not yet reached retirement age and have been a non-South African tax resident for an uninterrupted period of three years or longer, you can access your retirement and vested components in full. This will be considered a retirement fund lump sum benefit and will be taxed according to the withdrawal tax table that applies before retirement (see Table 1).

If I don’t need to access my retirement investments, can I leave them invested?

As a non-resident, you are allowed to remain invested in your retirement fund for as long as you like. By remaining invested, you will continue to benefit from tax-free growth and income within the product. You will only be taxed on the amounts you choose to withdraw from your savings component, or amounts taken as a lump sum benefit; either by using a cessation of tax residency withdrawal, or if you choose to retire from your retirement fund and take the allowable amount as a cash lump sum.

It is also important to note that if you retire from your retirement fund, you may be required to use a portion of your investment to purchase an income-providing product, such as a living annuity. The income that you earn from your living annuity will be taxed according to your marginal tax rate which is subject to the South African personal income tax tables.

Why do I pay tax on my South African retirement savings if I no longer live in South Africa?

Many countries, including South Africa, impose tax on the worldwide income of their tax residents and on the locally sourced income of non-residents. As your retirement fund is a South African source of income, you will be liable to pay tax on the income in South Africa, regardless of whether you remain a tax resident here or not. You may also be liable to pay tax on this income in your new country of tax residence, if they impose tax on your worldwide income. This may result in double taxation on your retirement fund income.

How do I avoid being taxed twice on my South African retirement fund income?

South Africa has entered into tax treaties with many countries to avoid the taxation of the same income twice. These double taxation agreements (DTAs) provide clarity on the taxing rights of certain categories of income and generally assign the taxing rights to only one of the two countries. Alternatively, they may allow for the income to be taxed in both countries and then cater for tax relief in the taxpayer’s country of residence for any taxes suffered by the taxpayer in the source country.

When assessing the taxation on your retirement fund, it is important that you refer to the specific agreement between South Africa and your country of residence for tax. Each of these agreements is individually negotiated and therefore the rules contained therein are unique to that specific agreement.

How do I know if a DTA will apply to my South African retirement income?

If there is a DTA in place between South Africa and your country of tax residency, the DTA can be applied to any retirement fund lump sums you take, as well as any living annuity income you earn. It is important to note that the DTA article which will be applied by SARS in assessing the South African tax implications of your income, will be based on the type of retirement fund you were contributing to while employed in South Africa. If your employer was contributing to a pension or a provident fund on your behalf, the “pensions and annuities” article in the respective DTA will apply, as the proceeds you receive from these funds are considered to be in consideration of past employment. Retirement annuities are not specifically linked to your employment and are considered personal retirement products. Therefore, if you wish to withdraw from your retirement annuity, the applicable article is the “other income” article.

Is it true that SARS will tax my retirement fund lump sum withdrawal up front, and that I need to claim the tax back when I file my income tax return?

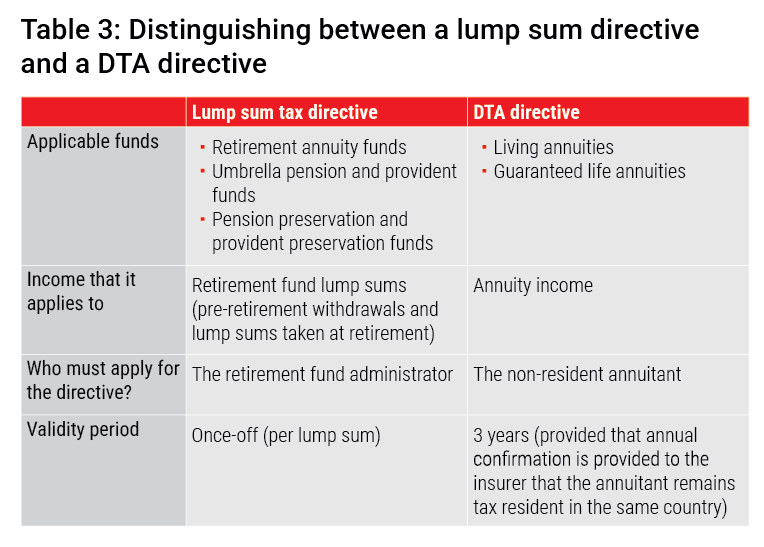

When you elect to take a retirement fund lump sum, your fund administrator is required to request a tax directive from SARS. This directive will stipulate the amount of tax the fund administrator is required to withhold and pay over to SARS on your behalf. We refer to this as a “lump sum tax directive”. If you are a non-resident member and South Africa has a DTA in place with your country of residence that assigns taxing rights to your country of residence, it is important that you inform your fund administrator that you would like them to request that SARS applies the DTA to the directive they will issue in respect of your lump sum payment. SARS will apply its discretion when assessing the applicability of the DTA in your specific case, and it may request additional supporting documents to aid its assessment. Should SARS determine that the DTA does not apply and instructs your fund administrator to withhold retirement fund lump sum tax, all is not lost, as you may still be able to claim relief in your country of tax residence for foreign taxes incurred in South Africa.

What are my options if I have reached retirement age?

If you have reached retirement age and wish to take your full retirement benefit in cash, you will still have access to a cessation of residence withdrawal, provided you have not yet elected to retire from the retirement fund. The tax implications of this withdrawal are as discussed above.

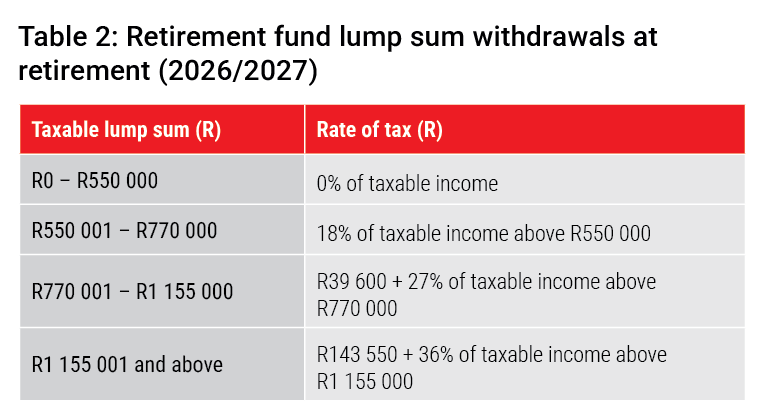

If you would rather elect to retire from the fund, you will be able to take the amount in your savings component, any harmonised vested benefits you may have, and one-third of the remainder of your vested benefits as a cash lump sum. The remaining balance must be used to purchase an annuity. The cash portion you elect to withdraw will also be treated as a retirement fund lump sum benefit but will be taxed per the retirement lump sum table applicable at retirement (see Table 2).

A DTA can also be applied to the lump sum benefit that you elect to take at retirement age, in the same manner described above. You will be required to inform your retirement fund administrator upfront, so that it can request that SARS apply the provisions of the DTA when issuing the lump sum tax directive.

The remainder of your retirement benefit must be used to purchase a qualifying South African annuity.

What are the tax implications of transferring my retirement investment to an annuity?

As a non-resident investor, you are not obligated to withdraw the full value of your retirement fund before reaching retirement age, nor are you required to take a portion of your retirement savings in cash once you reach retirement age. At retirement, you will be required to transfer a portion of your retirement investment to an annuity product, such as a living annuity or guaranteed life annuity, which will provide you with an income during your retirement. Legally, a South African retirement fund investment must be transferred into a South African annuity product. This annuity cannot be transferred to a non-South African service provider. The income that you will receive from your annuity meets the definition of employee remuneration according to the provisions of the Income Tax Act, and as such, your administrator is legally required to withhold employees’ tax from the amount paid to you, in the same way that a South African employer would pay a salary to you, net of employees’ tax, while you are employed.

Again, as this amount will be taxed in South Africa (at source) and will likely also be subject to income tax in your country of tax residence, you may be liable to pay tax on the same income twice. As this is the very reason that DTAs have been negotiated and agreed upon between tax administrations, you can apply for tax relief through a DTA directive from SARS. The DTA article that SARS will use to assess the extent of the relief applicable will be based on the retirement fund that you contributed to when saving for retirement (i.e. the original source fund of the retirement savings). The “pensions and annuities” article will apply where you contributed to and retired from an umbrella fund, and the “other income” article will apply where the annuity was funded from a retirement annuity.

How can I request my annuity administrator to apply DTA relief on my annuity income?

The process to apply for DTA relief on annuity income is slightly different in that you will be required to apply to SARS in your personal capacity. The process is detailed on the SARS website and begins with the completion of the RST01 – Application by non-residents for a directive for relief from South African tax for pensions, annuities and savings withdrawal benefits in terms of a DTA application form on your eFiling profile. Should SARS assess that the income from your annuity should be exempt from South African income tax, they will issue the relevant administrator with an instruction (i.e. a DTA directive) to apply a reduced rate of employees’ tax to the annuity income paid to you. It is important that this SARS letter is addressed to the long-term insurer, as the instruction is effectively providing the fund with assurance that it has been released from its legal obligation to withhold employees’ tax. This directive will be valid for three tax years, provided that you can provide your administrator with proof that you remain a tax resident in the same country each tax year. If you change your country of tax residence during the three-year period, the DTA directive immediately becomes invalid from the date of the change.

Consider professional tax advice

Navigating the complexities of your tax obligations across more than one country can be daunting, especially when you are not physically present in South Africa. Consider enlisting the services of a suitably qualified South African tax practitioner to act as your agent in South Africa, manage your tax affairs and assist you in obtaining all necessary supporting information, as required by retirement fund administrators and SARS.