The recent performance of South African bonds – which have outperformed cash and equities over three and five years – has prompted investors to ask whether they should consider rotating out of equities into bonds. Furthermore, the bonds versus equities trade-off is unusually difficult at present due to the very high real yields being offered by South African bonds, but at a time when the negative potential effects of a downgrade could affect bond prices. So, what should you make of it all? Londa Nxumalo tackles this question.

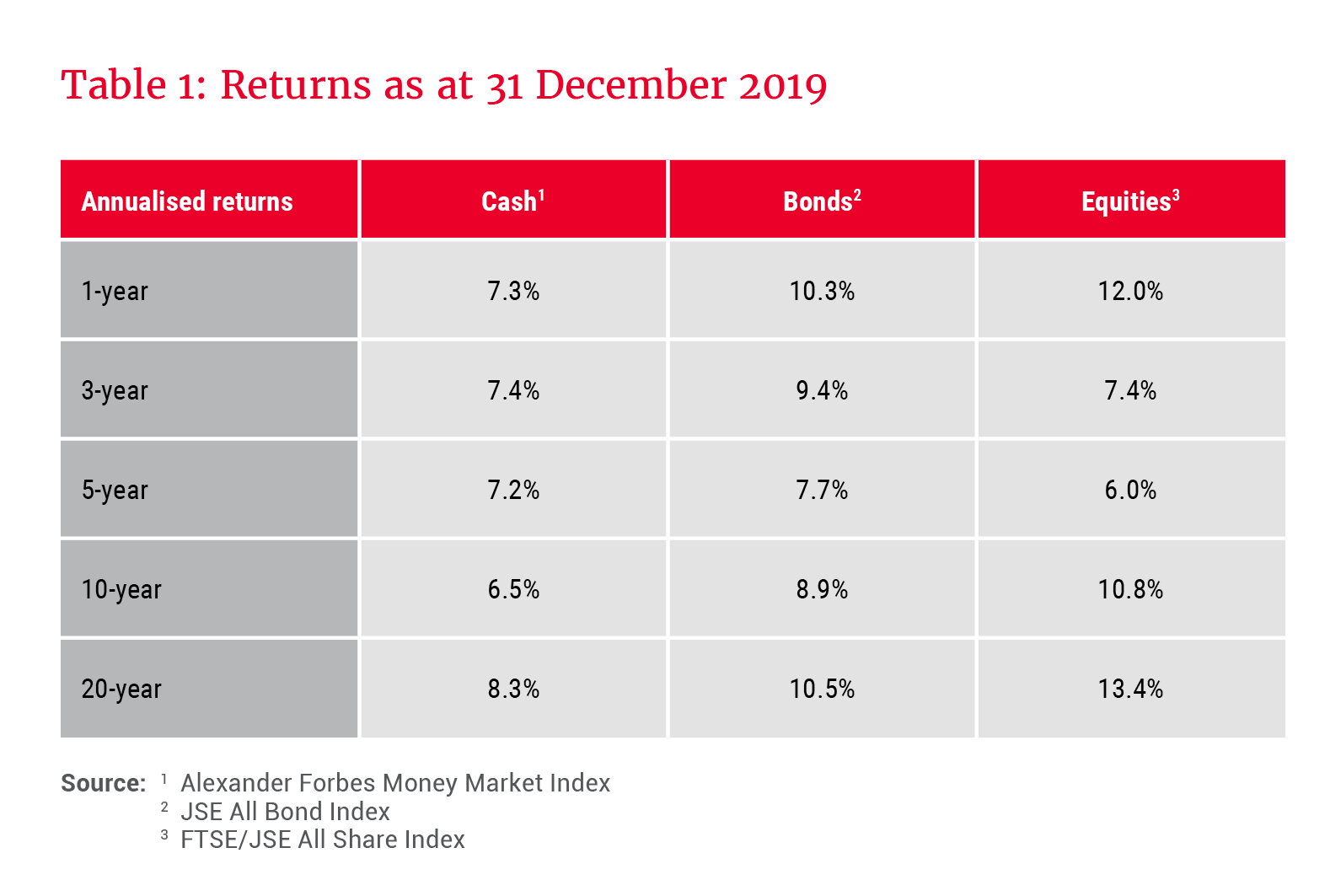

When assessing asset classes, it helps to consider your intended time horizon, as results may differ as you move your goalposts out. Unsurprisingly, equities have been the best-performing asset class over the long term. From December 1999 to December 2019, an investment of R100 would have grown to R492 had it been put into cash investments, R732 had it been invested in bonds and R1 244 had it been put into equities. See Table 1.

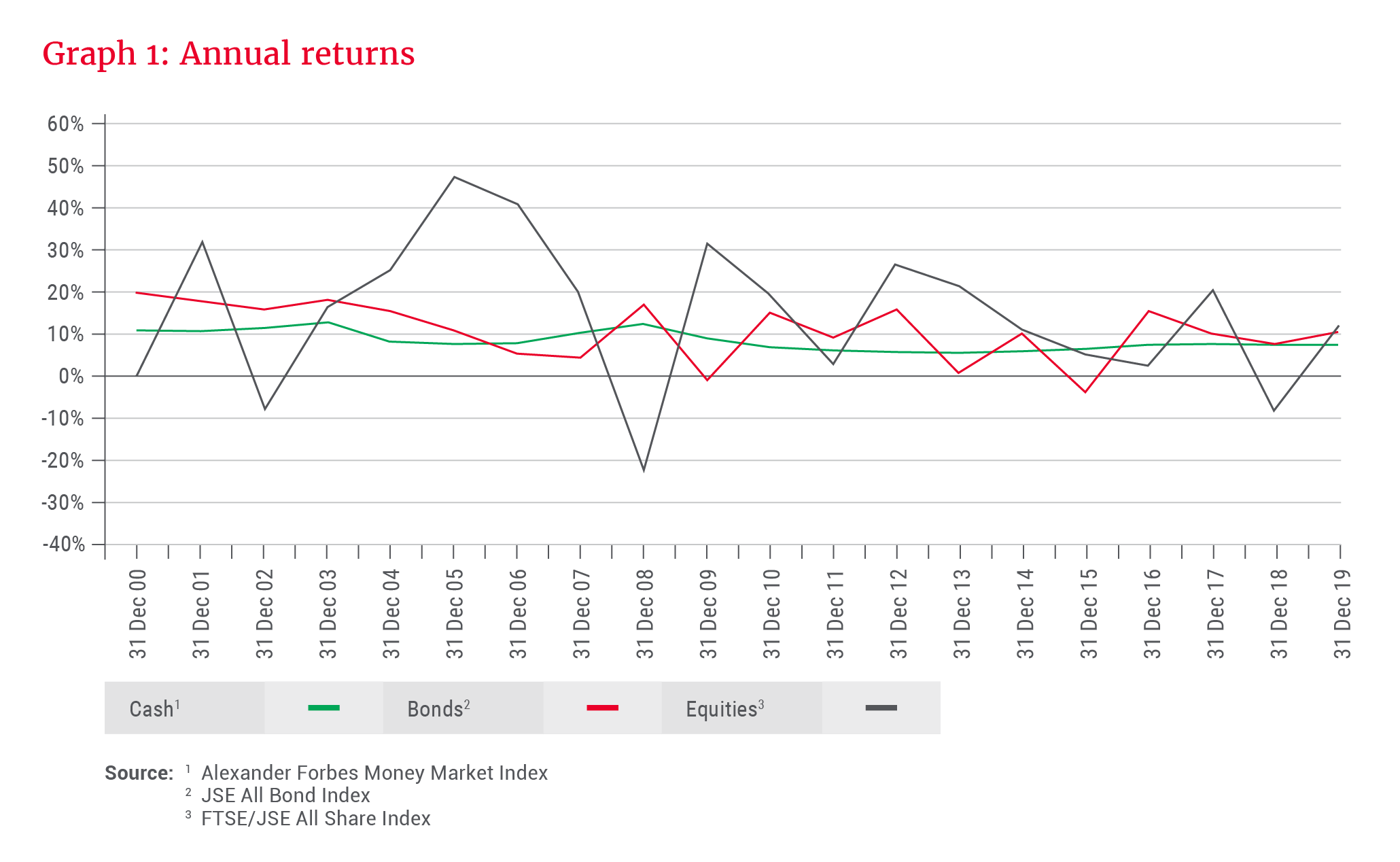

However, equities are more likely to have significant variations year-on-year, and investors must be cognisant of this. While bonds experienced two years of negative returns in the 20-year time period shown in Graph 1, equities had three negative years – with much larger losses. Cash returns have proven to be the least variable, while bonds have been more volatile than cash but less volatile than equities.

Volatility, or how much returns vary over time, is a measure that investors should consider based on their tolerance for variability. Equities have offered the best return over the long term, but this has come with higher volatility. Cash has had the least volatility but has also given the lowest returns. Bonds, on the other hand, have been less volatile than equities but have provided better returns than cash. This would indicate that it is a good idea for investors to have at least some allocation to bonds in a diversified portfolio.

it is a good idea for investors to have at least some allocation to bonds in a diversified portfolio

How much of one’s portfolio should be invested in bonds?

How much of a portfolio to invest in bonds depends on your time horizon and appetite for volatility, which are related. An investor with a longer time horizon can arguably tolerate greater variations in year-on-year performance (as long as the overall trend is rising) compared to an investor with a shorter time horizon, where earning a return while minimising variations – especially to the downside – becomes more important.

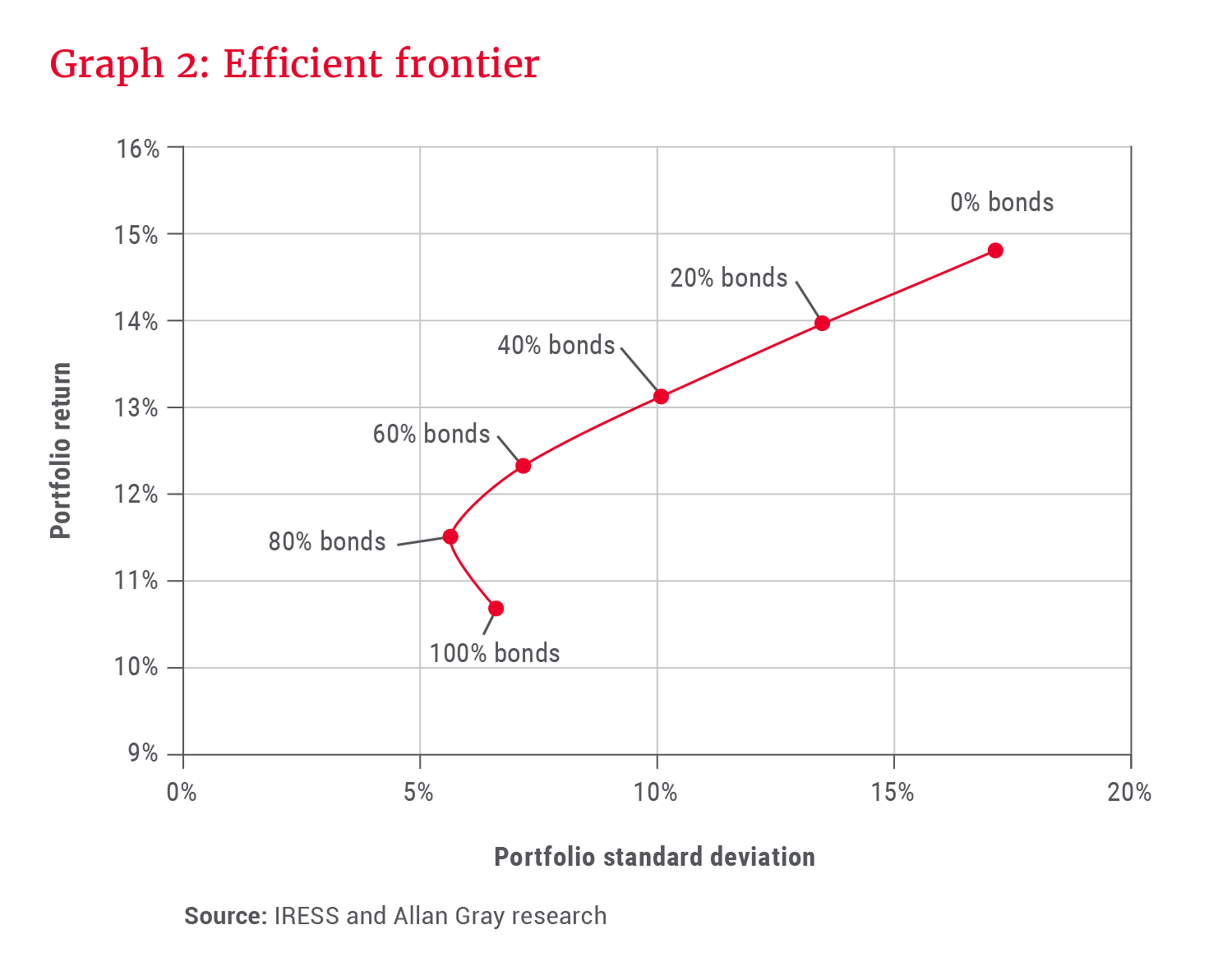

The efficient frontier, which is a theoretical portfolio optimising returns and volatility and shown by the line in Graph 2, illustrates the trade-offs of various bond/equity portfolio combinations, based on 20-year performance. The y-axis shows the average return, while the x-axis shows each portfolio’s volatility as measured by the standard deviation. One thing to note is that, while the efficient frontier considers all historic data, it does not consider the potential trade-offs at specific times given specific circumstances.

What can be seen from the efficient frontier is that having 100% in bonds would have resulted in a sub-optimal outcome, because allocating 20% towards equities (80% bonds) would have generated a better return with lower volatility. From that point onwards, increasing the equity allocation would have increased both volatility and returns. In summary, investors with a lower tolerance for variability should consider a higher allocation to bonds.

there is life after “junk” status

What happens if South Africa is downgraded?

It is important to remember that bonds are not entirely risk-free, and with the prospect of credit rating downgrades being a very real risk, investors must understand the potential impact on their portfolios.

South African government bonds are currently rated sub-investment grade (less generously called “junk”) by Fitch and Standard & Poor’s, which both rate South Africa BB+. Moody’s is the last major rating agency to rate South Africa investment grade, with a Baa3 rating – equivalent to BBB- at the other two agencies. However, Moody’s recently put out a negative outlook, meaning that a downgrade is probable within the next 12 to 18 months.

The significance of the Moody’s rating is that a downgrade would result in South African bonds being excluded from the FTSE World Government Bond Index (WGBI), an influential index tracked by many bond investors around the world. WGBI inclusion criteria require an investment grade rating from either Standard & Poor’s or Moody’s. A Moody’s downgrade would, therefore, result in forced sales by index trackers and other investors whose benchmark is the WGBI. The South African Reserve Bank (SARB) estimates that possible outflows emanating from a WGBI exclusion would range from R74bn to R118bn.

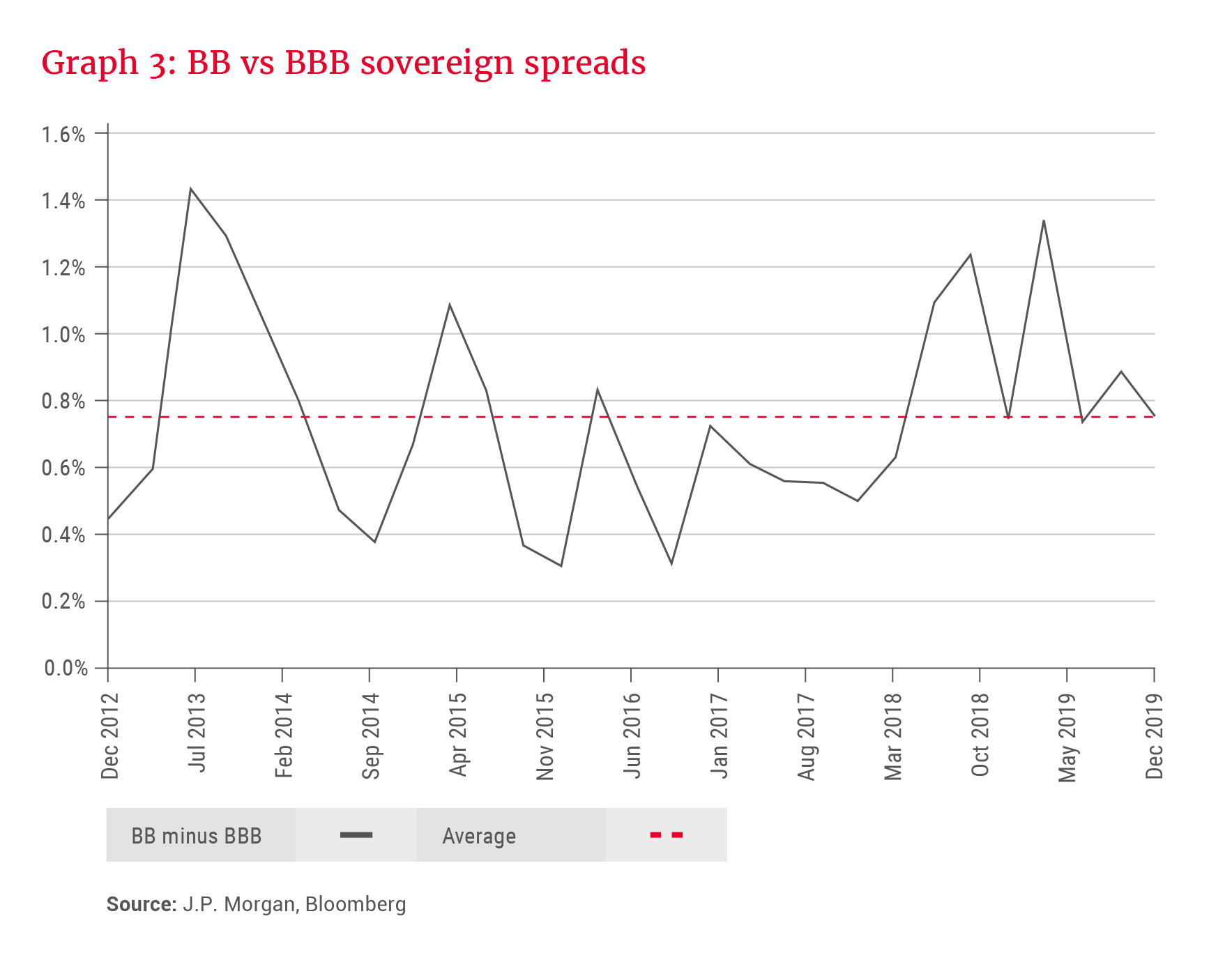

If the SARB is correct, a Moody’s downgrade would initially cause a sharp bond sell-off due to 3% to 6% of stock being dumped in the market. After the initial sell-off, one would expect bond yields to stabilise at a higher level consistent with a less creditworthy borrower. A simplistic way to guestimate how high is to look at the spread between BBB-rated and BB-rated countries, which is currently 0.75%. See Graph 3.

If the JSE All Bond Index (ALBI) duration is 6.8 years, a 1% increase in yield would result in a 6.8% decline in bond prices. If Moody’s downgraded South Africa today, and the ALBI yield rose from 9.2% to 9.95% to reflect the lower rating, this would result in the ALBI losing 5.1%. On the other hand, South African real yields are currently higher than their long-term averages, reflecting elevated tail risks from an unabated deterioration in government finances. An argument may be made that investors have already priced in a downgrade, and therefore bond prices may not move at all after the event.

Conclusion

Bonds offer an opportunity to diversify a portfolio, with the amount allocated towards bonds being inversely proportional to each investor’s time horizon and appetite for volatility. South Africa is facing profound macroeconomic challenges, and the threat of a downgrade by Moody’s to sub-investment grade is significant and could negatively affect bond prices. However, this may be priced in already and there is life after “junk” status. South Africa’s deep and liquid financial markets and a captive savings pool provide a floor for bond prices, and the foreign investor base would not disappear entirely if global conditions remained conducive for offshore investors to find emerging markets attractive. If inflation remains well-behaved (the SARB’s midpoint target is 4.5%), higher bond yields would provide attractive real returns for bond investors. The timing and the uncertainty of a pending downgrade mean that while bonds offer an opportunity to diversify a portfolio and generate real returns, investors should be cautious at this time.