The world is changing extremely fast. The global business shutdown is unlike anything seen outside wartime. It is impossible to know the length or depth of the coming recession and the time it will take for the coronavirus crisis to pass. That said, the global efforts to find solutions, whether a vaccine or the best protocols to reduce transmission, are enormous. Certain Asian countries, most notably South Korea, seem to have kept the number of infections under control, but it is difficult to know at what economic cost. Andrew Lapping provides some insights into the current crisis, its impact on the market, and what we are doing to position your portfolios for a range of future outcomes.

Asset prices have fallen sharply. The 30% drop in global equity markets is the fastest since 1929. South African assets have done particularly poorly. The FTSE/JSE All Share Index (ALSI) is down 27% year to date in rands and 38% in dollars, while the JSE All Bond Index is down 8% year to date. The fall in local bonds contrasts starkly with the moves in developed market government bonds, which have rallied sharply.

We hold platinum exchange-traded funds (ETFs) in our funds to diversify risk and add downside protection. Nevertheless, even the rand price of platinum has dipped 19% year to date, as precious metals have not been spared.

There are many scenarios that may play out. To my mind we are likely to experience inflation and weakness in developed bond markets as countries struggle to fund their rescue/stimulus packages. We are carefully buying assets that we think are undervalued. However, we are also cautious, investing in businesses that we think will survive. Unfortunately, in this environment there will be a great number of business failures.

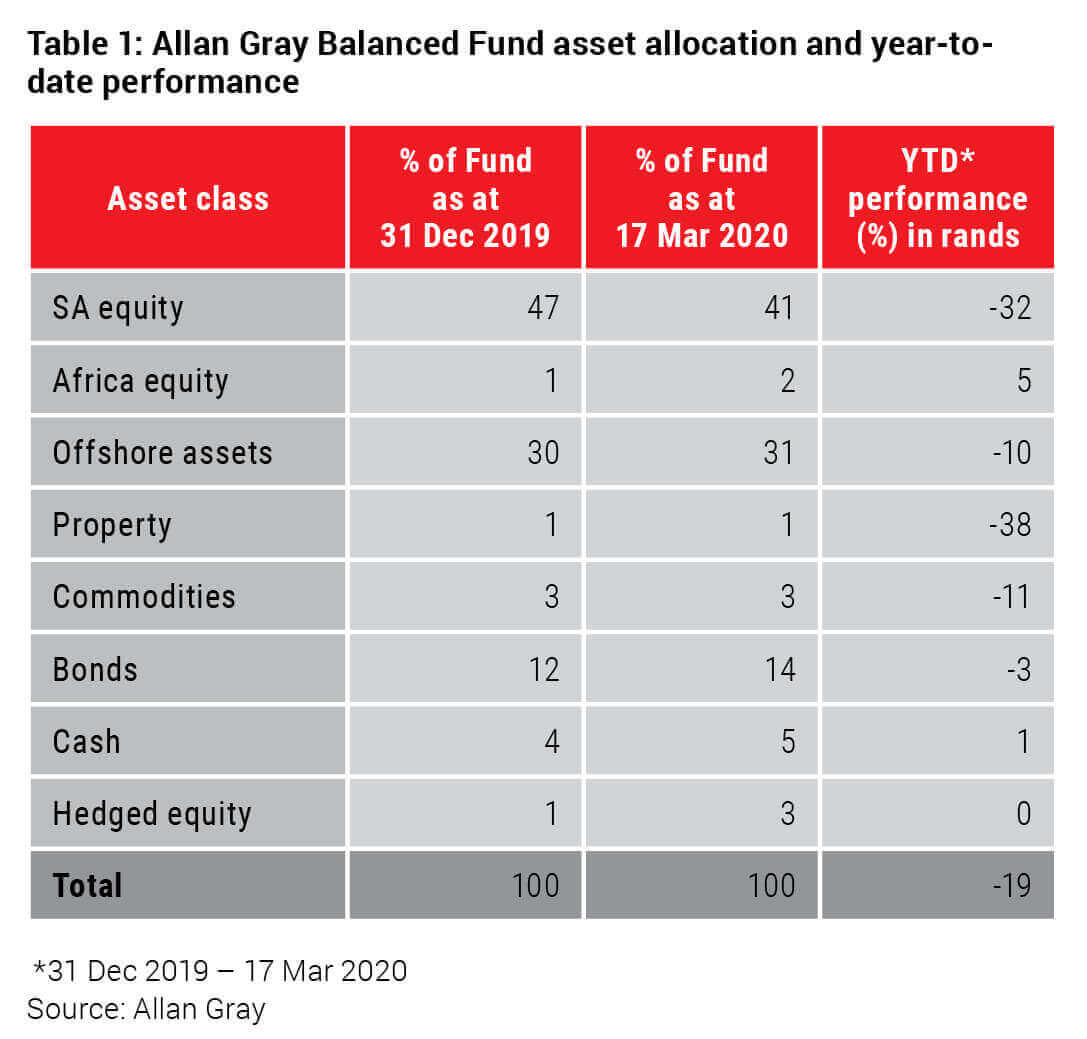

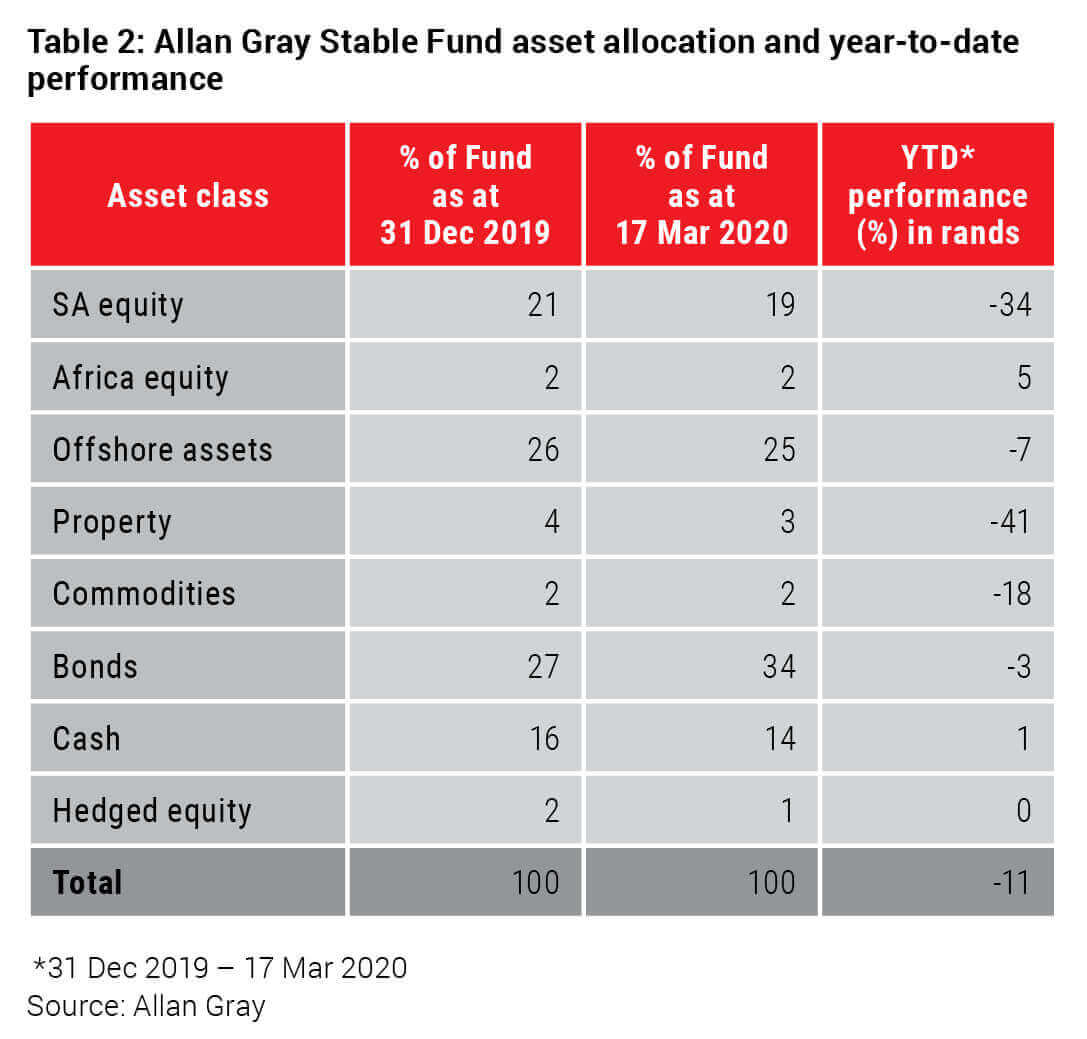

Below I address the asset classes that have driven the price moves across our funds, as well as the performance of certain of our large holdings (see Tables 1 and 2). Prices are extremely volatile day-to-day, but the aim of this note is to provide context to help you make sense of your portfolio at this very disconcerting time.

Rising long-term interest rates impact local bonds

The All Bond Index is down 8% since the start of the year. The cause of the loss is not a default, but rather rising long-term interest rates. The R2037 yielded 9.85% in January, for an attractive real yield of 5.5%. There was (and still is) a strong case for bond yields to move lower, given the low inflation rate and probable interest rate cuts, in which case locking in interest rates of 9.85% would be a great investment.

The distress in global markets has caused investors to flee emerging markets like South Africa, selling everything they can. This liquidation has caused the yield on the R2037 to sell off to 12%. Unfortunately, the yield gets to 12% by the price falling. Was the purchase at 9.85% a mistake? For sure it would have been nice to buy the entire position at 12%, but I think in time 9.85% will prove to be a good buying price. The Reserve Bank focuses on inflation and has kept the rate well controlled, below 6% for the past 15 years. If it can achieve this over the next 15 years, the R2037 will return 6% real at current prices – an exceptional investment.

Our inflation-linked bonds, a very low risk asset, have performed particularly poorly this year. In December and January, we were buying inflation-linked bonds at real yields of 3.6%. This is a government-guaranteed real return. These low risk assets have not been shielded from the current crisis. The R202 now yields a real return of 4.75% to maturity in 2033: while the price has fallen by about 10% to get from 3.6% to 4.75%. I believe the inflation linkers were a good buy at 3.6% and are now an exceptional buy at 4.75%. Holding the bonds we bought in January will still give a real return of 3.6% to maturity from the purchase date. The way to make a permanent loss is to sell them now, which we do not plan to do. We are steady buyers of both nominal and inflation-linked bonds at these yields. Time will tell, but we believe we are locking in good future returns.

A look at our local equity holdings

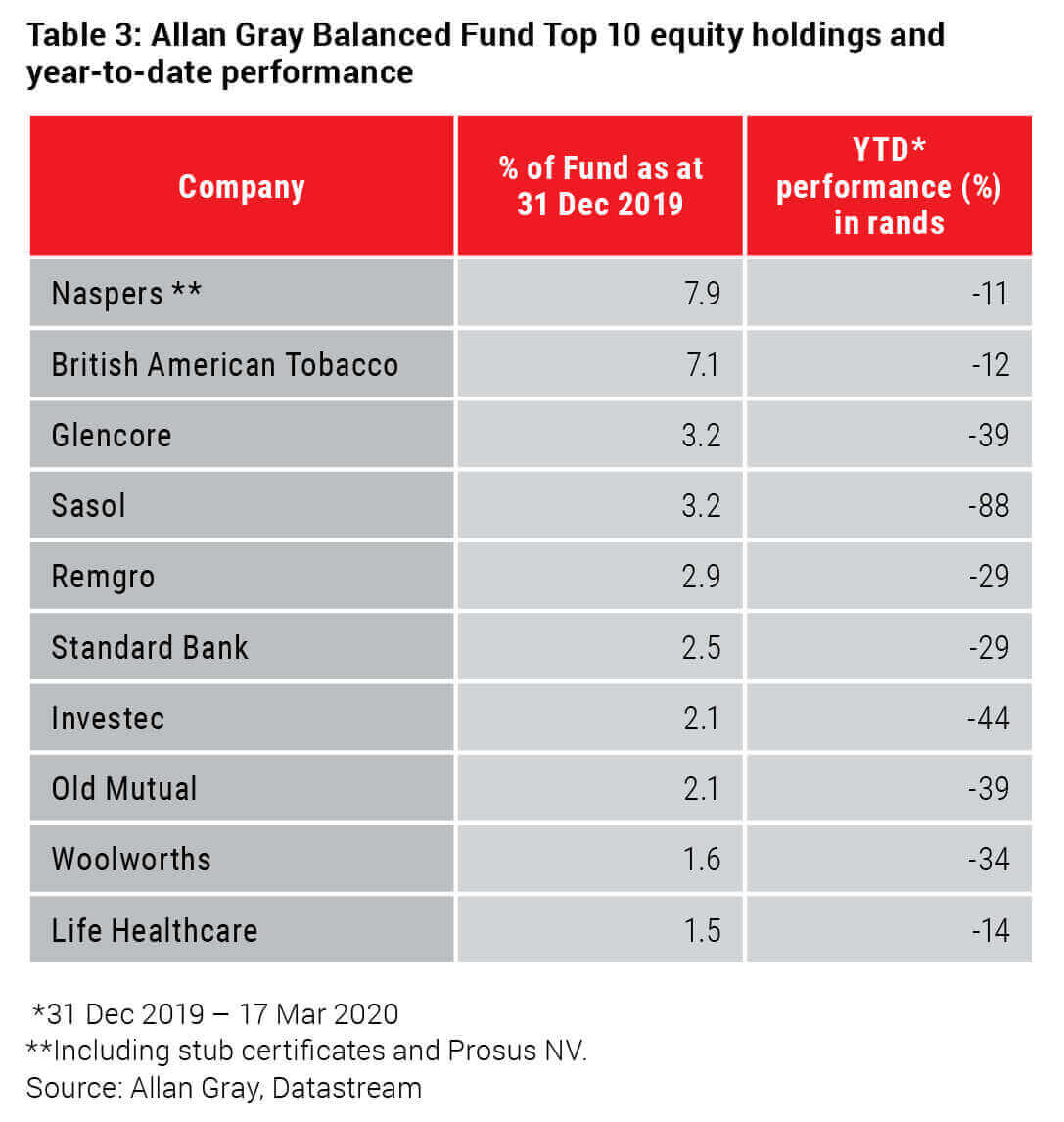

The biggest detractor by far has been our equity holdings, down ~33% year to date. See Table 3 for the equity holdings in the Balanced Fund. The important question to ask is whether these are permanent losses. Sasol’s price decline could be a permanent loss if the company can’t navigate the current oil crisis. It all depends on how quickly the oil price recovers and management actions. Very few would argue that an oil price of US$25, or even US$50 for that matter, is sustainable. Almost all oil companies are in severe distress: most are down about 75%, with the best performers like Exxon halving. Sasol is now small in the portfolio, at 0.5% of the Balanced Fund compared to 3.2% in January, but we still hold the share as we believe there is significant option value if the oil price recovers sooner than expected.

Do we have any other companies in the portfolio facing an existential threat? We have small positions in some hospitality companies, which are under pressure given the revenue collapse. However, those that survive the crisis offer huge upside potential.

Global banking shares have collapsed as investors price in extreme bad debts – and rightly so. The banking shares in our portfolio have suffered similar selling pressure. I think it is unlikely that governments will let their banking sectors collapse because of a government enforced shutdown. South African banks may not receive bailouts, as I am sure many developed market banks will, but our banks have good profitability buffers and are better placed than they were heading into the global financial crisis (GFC), when credit extension had been aggressive. The banking shares in our portfolio are priced for significant distress: Standard Bank trades on a price-to-earnings (PE) multiple of 5.9, which compares to the Nenegate low of 8.5, and the GFC low of 6.7. The last time the PE rating was at this level was in 1988. Similarly, Nedbank’s 12.7% dividend yield compares to the previous high of 9.5% in 2009. We believe the banks will survive this crisis and reward those investors who remained invested.

Commodity companies like Glencore are clearly sensitive to a demand collapse, but we think Glencore is well placed to survive. Yes, it has debt, but it does not have significant near-term maturities and does have very substantial liquidity to tide it over.

As equity prices fall, we are taking the opportunity to steadily and carefully invest the portfolio in very undervalued companies which we think will survive.

Global bonds continue to look overvalued

One of the few global asset classes to appreciate year to date is developed market government bonds, as investors have rushed to perceived safety. We do not own these assets as we believe that the enormous fiscal deficits that will come from the current crisis could very well lead prices in this asset class to collapse. Orbis, our offshore partner, is following a very similar approach to us and accumulating undervalued assets.

A look at the local currency

The rand is 20% weaker year to date. This, together with South African assets underperforming, has presented the opportunity to steadily repatriate money from offshore to buy local assets. Yes, the South African economic situation is worrying, but it is important to remember that currencies are measured relative to each other. The economic and debt situation is similar or worse in many developed economies and the rand has depreciated against those currencies, most particularly the dollar.

Where to from here?

The term uncertainty is overused. But where we stand today, the global outlook is truly uncertain. Economic activity is grinding to a halt, job losses will be enormous and the humanitarian impact of the coronavirus crisis is great. We are looking to invest your funds in a range of undervalued assets that should survive. Volatility will be extreme, but we are staying calm, looking to take advantage of opportunities that arise.

Historically the best course of action in times like these is to remain invested, painful as this may feel. You still own the same businesses you owned three months ago; the prices of those businesses are just 33% lower. When we bought these companies on your behalf, we were buying them for earnings and dividends they would generate over the next 10 years, not the next 12 months.

By the time you read this no doubt there would have been further changes – some of which are unpredictable. While it is increasingly difficult to remain rational when the world seems to have been knocked off its axis, we remain focused on steering you through the turbulence and making considered long-term decisions.