As we look at opportunities around the world, one thing seems clear – it is no time to be a hero. According to Alec Cutler, from our offshore partner, Orbis, overall markets appear plenty risky but insufficiently fearful.

Fear and risk in the market tend to move in cycles. As exciting as investing is, things aren’t as exciting when fear and risk are aligned. These environments tend to offer decent opportunity sets to active investors, but not extraordinary ones. The best opportunities arise when investors are afraid, but there’s far less than usual to be afraid of – times like November 1987, or years 2003 and 2009. Such periods offer target-rich environments for analysts, but require investors to swallow a lot of fear and recent bad experience in order to pull the trigger.

Now is not one of those times. As we look around the world, we see plenty of risks. Stock and bond markets remain expensive by absolute and historical standards. The US government has pulled every available lever to prod the economy and keep asset prices high, and central banks are (or are thinking about) pulling back from their unprecedented money printing experiment. They are trying to keep the global economy in a “Goldilocks” balance of good growth and low inflation – but that balance seems to be on a razor’s edge. Too much accommodation risks runaway inflation, and removing accommodation too quickly risks causing a recession. And there is also a fourth possibility that many investors are too young to remember: stagflation, or poor growth and high inflation.

In addition to these economic risks, conflict continues to simmer in the Middle East, a trade war looms between the US and most everyone else, inequality is spurring inflationary, globalisation-killing populism and nationalism, and technology is changing society in ways we don’t fully understand. Risks appear high.

Yet by most measures, investors are optimistic. As one indicator, consider the Volatility Index (VIX) – the “fear gauge” of implied volatility in the US stock market. Amid the unusual stability of 2017, the index was often below 10, which is unprecedented. When markets dived in February, it briefly spiked above 40. To us, that looked like a healthy shift!

But it fell back to 12 in early June, against a long-term average of 20. Meanwhile, retail investors’ margin levels are high, and the cash levels of institutional investors are low. Investors remain sanguine, and high risk and low fear make a dangerous cocktail.

Scenario analysis

While we do not make big macro forecasts, we cannot stick our heads in the sand either, so we look at multiple scenarios and assess how the portfolio might behave in each of them. Rather than betting heavily on any one scenario, in assessing risk in the por tfolio we aim to ensure that our positioning isn’t disastrous in any of the scenarios that appear most plausible. We are not economists – nor do we want t o be or think that would be beneficial.

To minimise bias, our risk team models the portfolio’s performance under a range of assumptions so that we can understand how the portfolio might behave in the scenarios we are most concerned about. Most of our market risk scenarios come from a couple of pretty simple observations: 1) What are valuations telling us, and 2) what is everyone else worried about? We’ll tend to worry more about things that others are not worried about.

This approach tends to work over time because fear and valuations are linked. If everyone is worried about the same risk, that fear is likely priced into markets, making the feared outcome both less likely and less rewarding to guard against. In February 2016, for example, investors’ top fears were deflation and full-blown global recession, so we weren’t surprised to find plenty of undervalued securities among inflation and economic growth beneficiaries. In the February just past, the top fears were inflation and a bond crash. What a difference a couple of years makes. Investors now seem to expect continued growth. That makes us nervous, and inclined to worry more that recession may be closer than believed.

The old playbook

There is a classic playbook for environments like this: Shift out of cyclical shares like industrials and banks, and into defensives such as consumer staples. This time, however, defensives aren’t attractively valued.

While many investors view consumer staples as extra safe stocks, we think they are more like extra risky bonds at their current valuations. Earnings and revenue growth for the likes of Nestlé, Coca-Cola or Procter & Gamble have been next to nothing over the past 10 years, and today, these shares offer dividend yields of a few percent. No growth (despite a decent economic backdrop) and a few percent yield sounds a lot like a low-yielding bond.

Short-term US Treasury notes provide an attractive alternative. They offer 2.3% yields, with essentially no interest rate or stock-related risk. In our view, these beat out the most attractive consumer staples in the equity market. As some of our favourite cyclical shares have performed well and returned to fair value, we have rotated some of the capital in the Orbis Global Balanced Fund out of those stocks and into short-term US Treasuries.

While attractive equity opportunities are harder to find when fear is low and risk is high, there are about 8 000 investable stocks globally, and our research team continues to find attractive opportunities. Two types of shares provide particularly good illustrations of what we’re finding in the current environment: beta-arbitrage opportunities, and our wide footprint of idiosyncratic holdings.

Beta arbitrage

Benjamin Graham and David Dodd are the godfathers of value investing. Their basic advice: Buy shares in great businesses when they are temporarily thought not to be so.

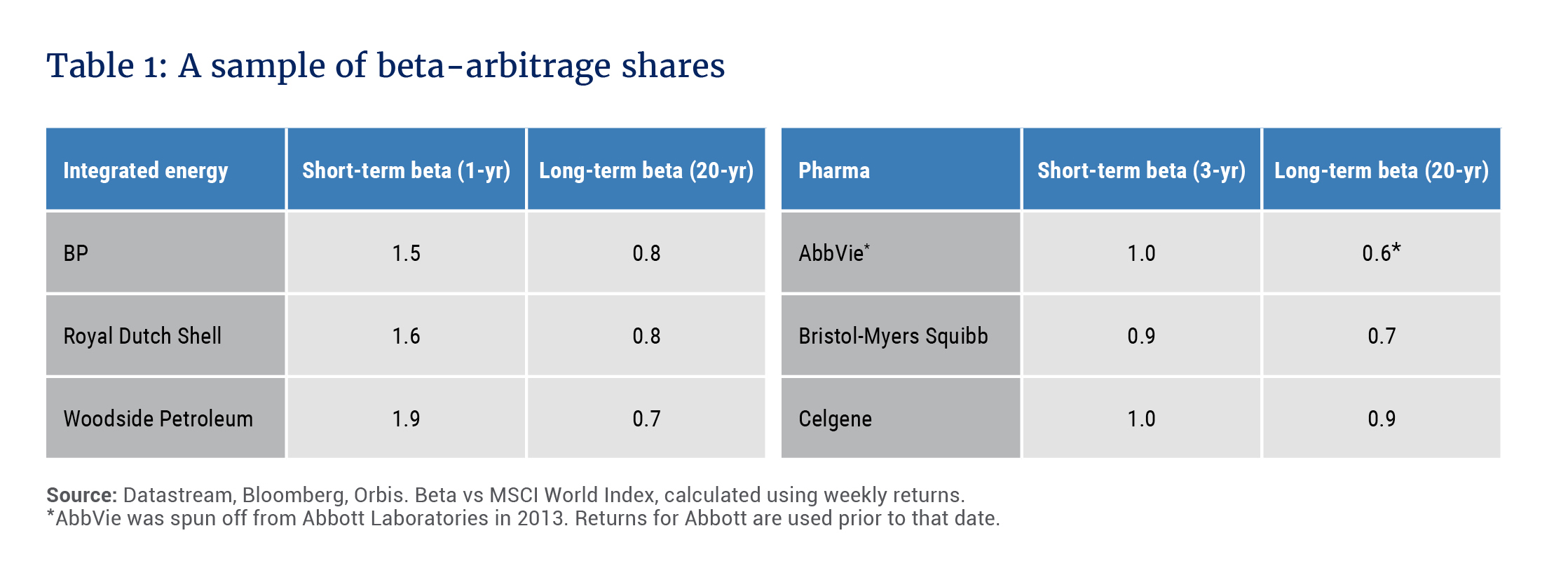

In the Orbis Global Balanced Fund, we have found a moderate risk corollary: Buy shares in safe businesses when they are temporarily thought not to be so. At the Fund’s inception, we bought telecommunications shares when the market seemed to forget about their stability. Over time, they were once again seen as defensive, and the shares appreciated. We have also bought selected consumer staples with much the same thesis. As those rerated, helped by central banks suppressing bond yields, we rotated capital into integrated oil companies and then added selected pharmaceuticals.

A stock’s beta measures its market sensitivity. Simplistically, a stock with a beta of 1.2 is expected to move 1.2% for every 1% move up or down in the market. But the calculation period matters. When a sector is out of favour, its beta may increase, making it look more risky. When that happens, we find it valuable to consider how the near-term number stacks up against the company’s long-term average.

For our selected beta-arbitrage shares, as shown in Table 1, we believe temporarily high betas have tricked investors into thinking the companies have permanently lost their high-quality, stable fundamentals. If we are correct, the market will rediscover the stability of these companies and reward them by returning them to higher valuation levels. That doesn’t happen in a predictable way, as we’ve seen during periods of underperformance of our integrated energy names over the past few years. But as we wait for the market’s reappraisal, the low valuations and high dividend yields of our beta-arbitrage names should make them resilient in the face of a market decline.

Idiosyncratic opportunities

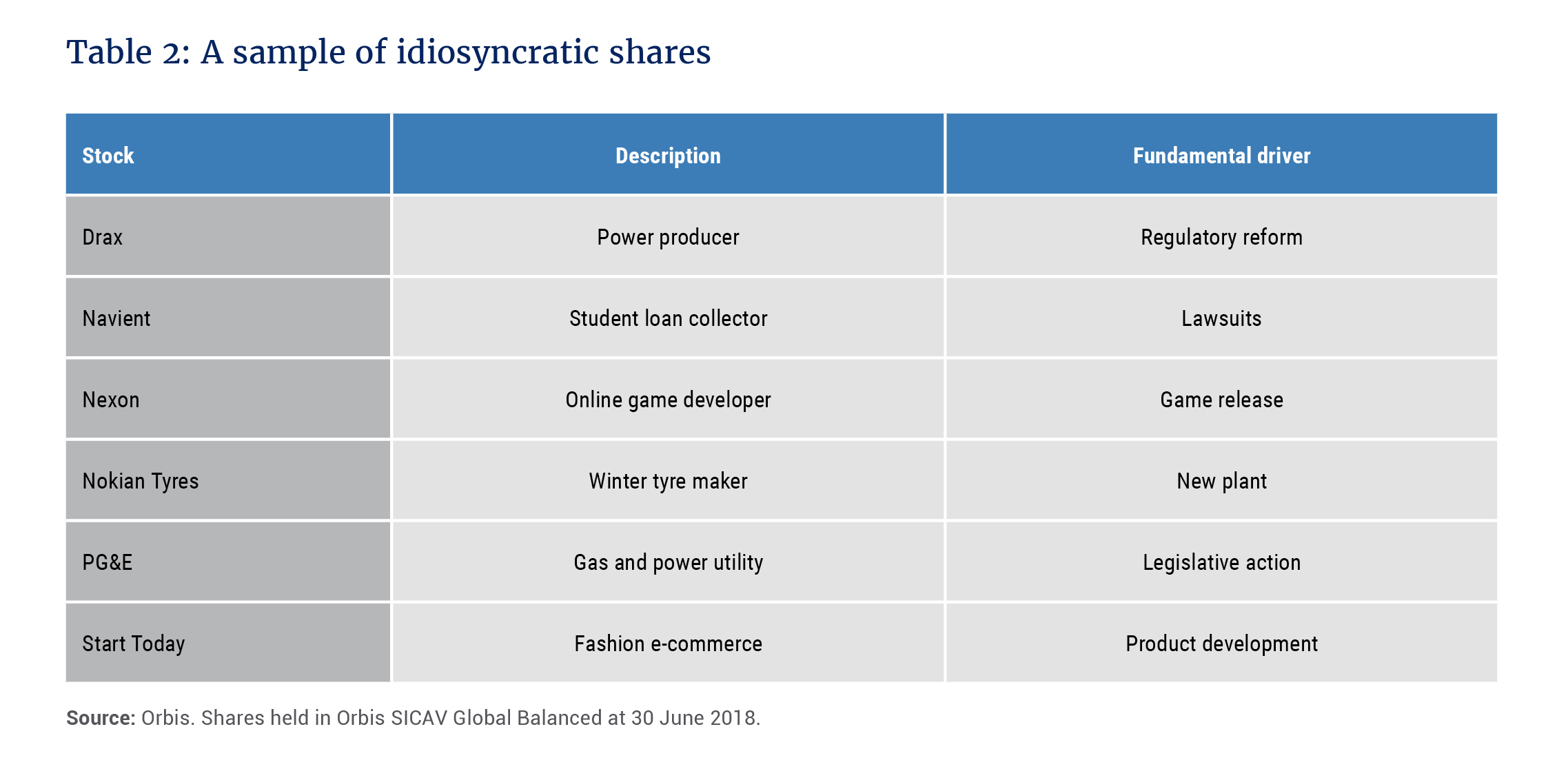

Investing in attractive opportunities that have very little to do with the economic cycle is another way to deal with the risk of the economic cycle rolling over. Table 2 gives a sample of these names.

Drax is a UK biomass and coal-fired power producer. The UK is trying to cut out coal in favour of wind and solar, but the resulting stretched capacity has led to winter outages in some regions. The country needs reliable power, and Drax can provide it efficiently. It has transitioned most of its units from coal to wood pellets, a renewable source of energy, and is seeking to switch other units from coal to a highly efficient type of gas generator. Both are excellent sources of baseload electricity, but get little positive attention from politicians and regulators, currently enamoured by less reliable solar and wind power schemes.

Drax has highly visible cash flows through 2027 that more than cover the company’s entire stock market value and net debt, and we think Drax will continue to have a valuable role to play after that date. And importantly, the company’s success or failure has almost nothing to do with overall market valuations, or the economic cycle. It is idiosyncratic.

The same is true of other shares such as Nexon, which is due to launch a mobile version of its blockbuster game Dungeon & Fighter, and Navient, which is being sued for how it went about administering student loan payments on the US government’s behalf. Each of these companies has risks, but uncorrelated risks that we believe are more than accounted for in their valuation levels, and by combining them, we can hopefully accrue the long-term gains that come from buying on the cheap while diversifying down the overall risk.

Staying the course

In short, we are managing risk by doing what we always do: Hunting for attractively priced individual securities. It’s not an easy environment, but by focusing on bottomup opportunities, we believe we can provide an attractive balance of risk and return – without being a hero.