Understanding your investments, and the risks you may face when investing, can go a long way towards helping you successfully navigate trying times. Lydia Fourie explains.

The current economic environment is enough to tempt us to just keep our money under the mattress. Risk abounds: Inflation keeps landing on the wrong side of the South African Reserve Bank’s (SARB’s) target range; in turn, the SARB’s Monetary Policy Committee continues to hike interest rates to try and curb inflation, and the market doesn’t seem to know what to make of it all, with volatility being the only certainty. Who knows what the future holds? However, as risky as things may seem, now is probably the worst time to abandon your investment plans.

Inflation is the rate at which the cost of goods and services increases over time. As things become more expensive, you are able to buy less with the same amount of rands. In a rising inflationary environment, like we are currently experiencing, this effect is even more pronounced. If the return you earn from an investment doesn’t keep up with inflation, you are effectively losing ground.

Considering the lack of return, storing money “under the mattress” or in a regular bank account won’t provide you with enough protection against rising inflation – history has shown that you need exposure to risk assets, such as shares, to meaningfully beat inflation over the long term. This is because these assets have historically appreciated in value by significantly more than the inflation rate when measured over long investment horizons.

Given the need for exposure to risk assets, it’s important to get your head around different types of investment risk and to form an understanding of how much risk you can take on.

How does Allan Gray view investment risk?

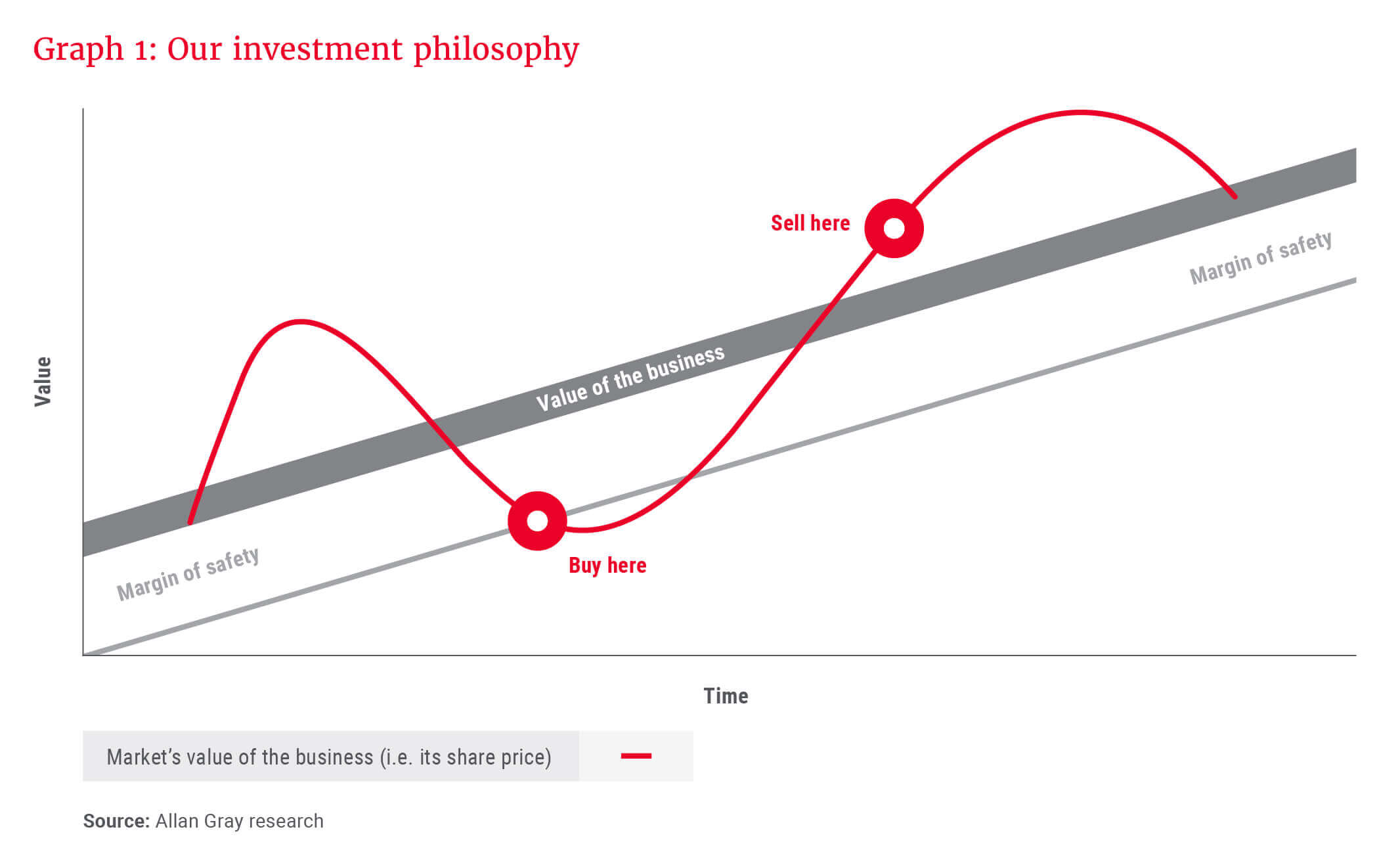

There are different definitions of investment risk. At Allan Gray, we define risk as the likelihood of permanently losing money from an investment.

Losing money is the main risk that we are concerned about and that we actively manage; we care about helping our clients preserve and create wealth over the long term.

Losing money is the main risk that we are concerned about and that we actively manage; we care about helping our clients preserve and create wealth over the long term. This is engrained in our investment philosophy. We buy shares we think are undervalued – with a margin of safety, as shown in Graph 1 – and sell them when we think they have reached their worth, regardless of popular opinion. This approach ensures that we don’t overpay for an investment. We also don’t get greedy when it comes to deciding when to sell; there is additional risk in hoping that a rising share price will continue past the share’s true value, which is why we are very disciplined about selling when it has reached our estimate of its true worth.

What are some other definitions of investment risk?

While the risk of capital loss is our primary concern, we acknowledge that not everyone views risk the same way. Investment risk is often defined more generally as the possibility that the actual return from an investment differs from the expected return or the benchmark’s return.

Another common definition is volatility. Volatility – or variability – is how much the value of an investment has fluctuated over time and is often used to suggest how volatile returns may be in the future. The more the historic value of an investment has varied, the higher its level of volatility, and vice versa. While we do not focus on these kinds of risks, we acknowledge that they introduce the biggest risk of all: behavioural risk.

If an investment performs differently from what you expected, you may be tempted to make changes to it or to withdraw. However, such decisions should always be well considered and aligned with your needs and objectives. Knee-jerk reactions may derail your plans and result in losses.

Similarly, if you find yourself unable to stomach the inevitable ups and downs associated with many investments, you may end up selling at the worst possible moment (i.e. after a big drop), thereby locking in a loss. This is why it is so important to understand the reasons why you are investing, and to ensure that your choices are appropriate.

How to compare unit trusts

Before selecting a unit trust, you must choose an investment manager. The right manager is one whose investment philosophy and process resonate with you. A philosophy indicates how the manager thinks about investments and informs the way that they invest. The process refers to how the philosophy is implemented practically when managing client portfolios. If you understand the manager’s philosophy and process, it should be easier to make sense of their investment decisions, leading to better alignment between their actions and your expectations.

Once you have chosen an investment manager, you can focus your attention on their range of unit trusts. The selection process can seem overwhelming, but there is a lot of information available to aid your decision-making. All investment managers are required to publish minimum disclosure documents for the unit trusts that they manage. These are often called factsheets, and they contain important information about the characteristics of the unit trusts.

When comparing unit trusts, look at things like the funds’ objectives, suggested time horizons for investing, volatility and fees. This information should be available on the factsheets or directly from the investment manager.

… you have to live through the short-term ups and downs and be disciplined enough not to jump ship at the wrong time.

It is important to choose a unit trust that matches your risk profile. Your risk profile reflects how much risk you are comfortable with. While we all have inherent preferences regarding risk, it is important to approach it rationally when it comes to your investments. Your investment horizon (how long you intend to invest for) is the biggest determinant of the level of risk you can afford to take, and you should make sure that it aligns with the investment horizon of your chosen unit trust. The more time you have, the more risk you should be able to tolerate, and the greater your chances of achieving your long-term expectations. This is because returns compound, and volatility tends to even out over time. The possibility to regain lost money is therefore linked to how long you can remain invested. If you invest in a more volatile unit trust (usually one with more share exposure), you need to be able to endure the fluctuations in the short term to reap the return benefits over the long term.

Choosing a unit trust that is aligned with your risk profile can help ensure that you stay the course and enjoy investment success, as you will have a better idea of what to expect from the investing journey.

How do these concepts play out in our unit trusts?

While we encourage a long-term approach to investing, we realise that the experience of investing doesn’t only happen at five- or 10-year intervals – you have to live through the short-term ups and downs and be disciplined enough not to jump ship at the wrong time. This is easier said than done, but looking at the longer-term picture can help to put things into perspective.

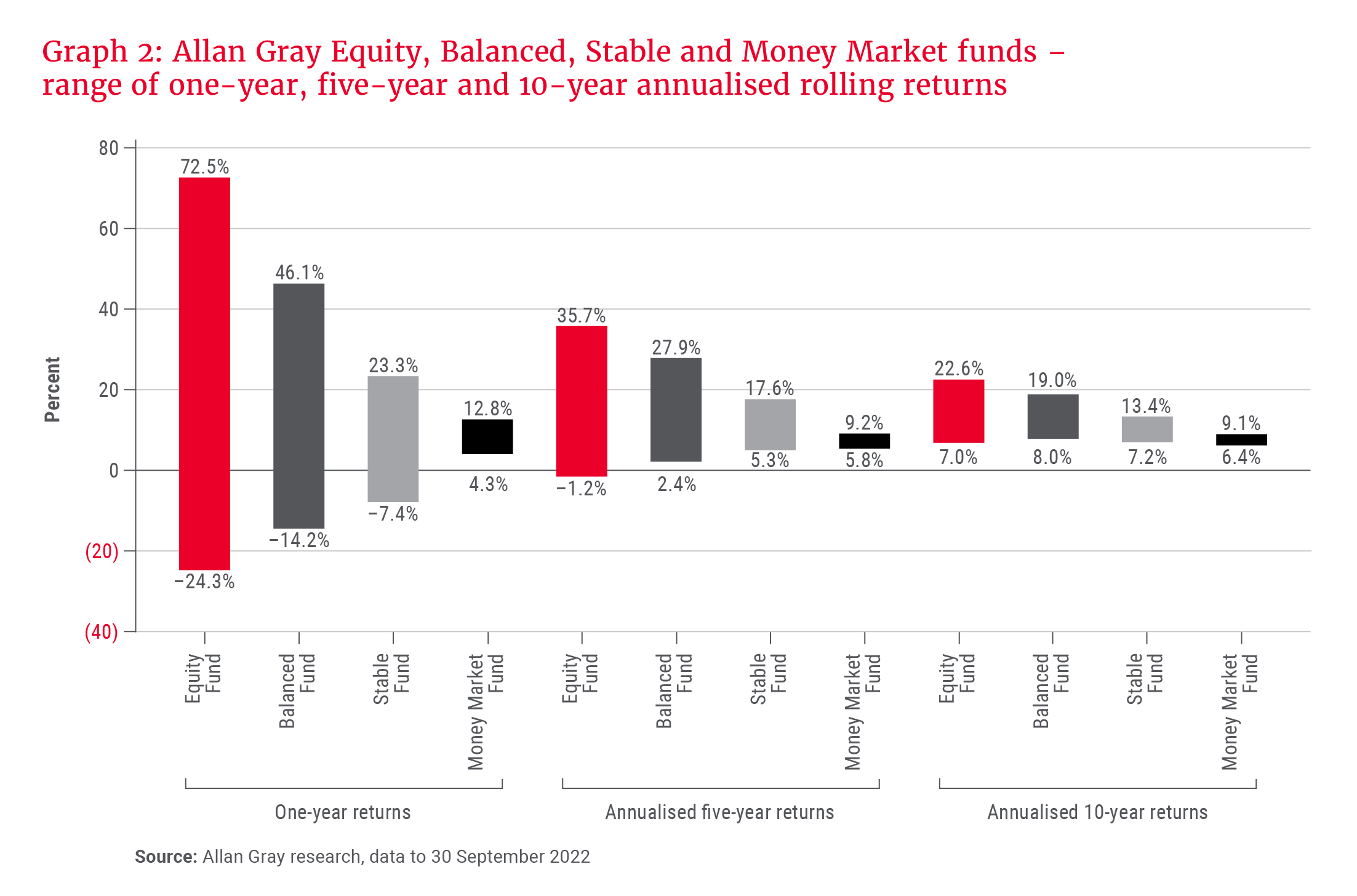

Graph 2 shows a range of past returns for the Allan Gray Equity, Balanced, Stable and Money Market funds using data for the period since inception of the Money Market Fund (the youngest of the four funds) until 30 September 2022. The graph contrasts the difference between the minimum and maximum one-year returns for each fund over this period with the corresponding difference for its annualised five- and 10-year rolling returns for all five- and 10-year periods included in the dataset.

The graph shows us two things: Firstly, the range of past returns is widest over the one-year time horizon for each of the four funds, i.e. the variability of returns is higher, as can be seen by the maximum and minimum returns being more extreme. Secondly, the range of past returns (the variability of returns) narrows when you move from the Equity Fund to the Balanced Fund, from the Balanced Fund to the Stable Fund, and from the Stable Fund to the Money Market Fund. This is in line with the characteristics and objectives of the funds.

The main takeaway here is that returns can be very volatile and extreme over the short term, especially in a unit trust with more share exposure. However, as the time period increases, the volatility of a fund’s returns tends to smooth out. Bearing this in mind can help you to endure the short-term fluctuations in performance.

Understanding is the first step towards better investment outcomes

It is important to take advantage of the information that is made available to you when choosing a unit trust, and to ensure that the characteristics of your chosen unit trust match your needs and objectives. Understanding the nature of your investment and what to expect while invested will ultimately lead to better long-term outcomes if you can remain invested through any short-term fluctuations.

If you do not have the resources, or lack the appetite to do your own investment research, it is a good idea to consult an independent financial adviser (IFA). An IFA can help you determine your risk profile and take a holistic look at your finances to recommend the best solution for your specific needs.